DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

VantageScore Solutions, a company that produces consumer credit scoring models, has found that 1-in-3 people in disadvantaged areas may not be able to obtain a credit score from a traditional credit bureau, but these people, whom number in the tens of millions, may be scoreable under more modern systems with inclusive methodologies.

VantageScore Solutions, a company that produces consumer credit scoring models, has found that 1-in-3 people in disadvantaged areas may not be able to obtain a credit score from a traditional credit bureau, but these people, whom number in the tens of millions, may be scoreable under more modern systems with inclusive methodologies.

The new internal research focuses on “the size and characteristics of these consumer populations and also breaks new ground to examine socioeconomic factors like income, race and other profile characteristics that contribute to a consumer’s likelihood of being ‘conventionally unscoreable,’ which is defined as those who lack the following information in their credit file: (1) at least one tradeline/account open and reported to the credit bureaus for six months or more; and (2) at least one tradeline/account that has been reported to a credit bureau within the past six months.”

VantageScore released the findings of their research in two parts; the first part of the research analyzed the conventionally unscorable population and how a more inclusive model, such as a private proprietary model, could bring these customers to the market and assign them a predictive credit score. The research tracked what these consumers score could have been in the 300-850 range.

The second part of the research examines the relationship between socioeconomic factors, the unscorability of some consumers in a traditional model, and how this affects consumers’ access to credit. This research also used income, education, race, ethnicity, home ownership, and access to banking services to explain how these factors explain the significant differences between them and a traditionally scoreable person.

Other key findings include:

- Income has the strongest effect on scoreability. Consumers in communities with low household income levels (less than $50,000) have less than 50% of the odds of obtaining a credit score with conventional models when compared to consumers in communities with higher household income levels (i.e., greater than $90,000).

- African American populations are particularly disadvantaged by the relationship between income and conventional scoreability because they tend to have lower income levels.

- After accounting for other factors, communities with higher African American and Hispanic populations experience lower levels of scoreability through the use of conventional models.

- Similarly, consumers living in areas with high renter rates or areas with more limited access to banking services have lower odds of obtaining a score with a conventional model, even after controlling for other factors.

“Broadly speaking, the studied socioeconomic factors have a compounding effect on various consumers’ ability to receive a credit score from conventional models, limiting access to credit and economic opportunity,” said Silvio Tavares, President & CEO of VantageScore. “Our research demonstrates how more inclusive models like VantageScore help to rectify inequalities that have persisted due to outdated legacy systems and processes, and assist in closing the scoreability gap for millions of consumers.”

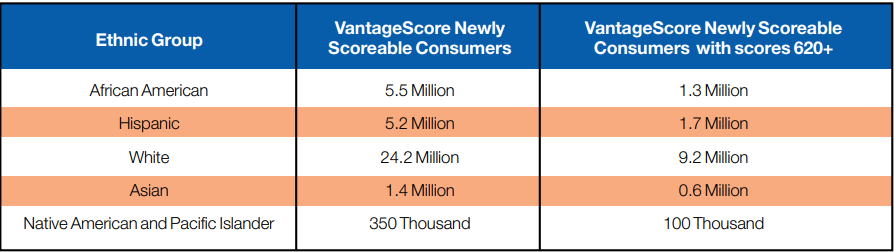

The amount of consumers that qualify a traditional credit score was found to be approximately 208 million people, but using a comprehensive proprietary model could give another 37 million consumers a score bringing the total of scoreable consumers to 244 million. VantageScore estimates that by using one of their models they can give 96% of the adult population a score

“The ‘newly scoreable’ population includes consumers with young credit files, consumers who do not have credit accounts but have other data on their credit files as well as consumers who have been recently inactive with credit,” VantageScore said. “African American and Hispanic populations, in particular, are negatively impacted by conventional scoreability criteria and they make up 10.7 million of the 37 million newly scoreable population; of those consumers, approximately 3.2 million have VantageScore credit scores of 620 and above.”