DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

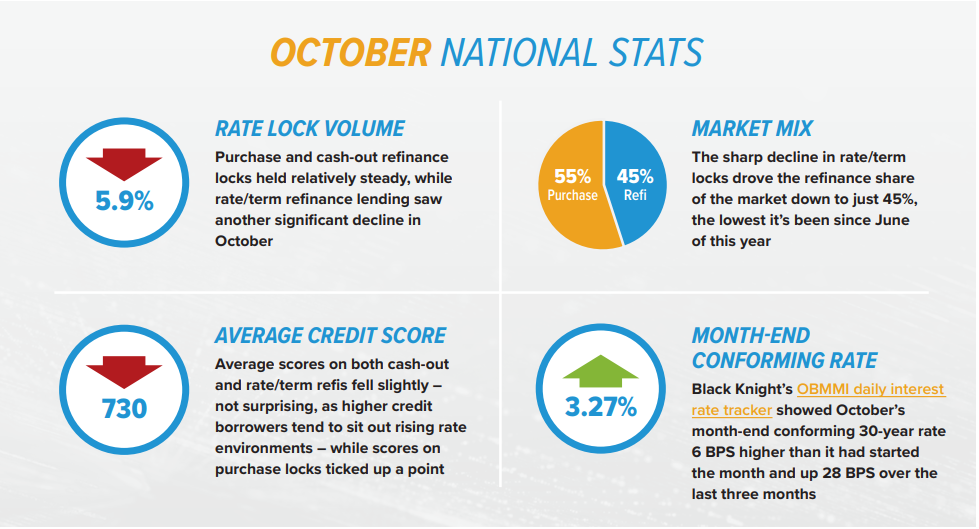

Black Knight Inc., has released the latest iteration of it Mortgage Monitor Report which looks at how rising interest rates affect the dynamics of the refinance lending market.

Black Knight Inc., has released the latest iteration of it Mortgage Monitor Report which looks at how rising interest rates affect the dynamics of the refinance lending market.

According to Black Knight Data & Analytics President Ben Graboske, historic refinance activity during the pandemic resulted in essentially tens of billions of dollars in economic stimulus.

“The record low interest rate environment driven by the nation’s COVID-19 response resulted in nearly 9 million homeowners initiating rate/term refinances over the first 18 months of the pandemic,” said Graboske. “Together, these borrowers reduced their aggregate mortgage payments by more than $1.3 billion per month, for some $14 billion in realized monthly savings to date. In fact—assuming they all stay in their homes for the duration of 2022—this group is on track to save nearly $35 billion in total by the end of next year. By nearly any measure, that is an extraordinary level of potential stimulus to the economy as a direct result of refinance lending.”

According to the report, recent rate increases have eliminated refinance incentive for 3.4 million mortgage-holders, but the population of 11.5 million remaining high-quality candidates is still larger than at any time prior to 2020. In the 18 months since the start of the pandemic, homeowners have reduced their mortgage payments by more than $1.3 billion per month through rate/term refinances, realizing $14 billion in savings to date. By the end of 2022, those borrowers will have realized nearly $35 billion in aggregate savings, with the potential for nearly $16 billion per year in continuing, ongoing economic stimulus.

As interest rates rise, 5.5 million took advantage of market conditions to tap into their equity by taking out a cash-out refi, which now makes up the majority of the refi volume.

“Keep in mind, that’s on top of the $322 billion homeowners tapped via 5.5 million cash-out refinances during the same period. More than half of the nation’s $9.1 trillion in tappable equity is still held by homeowners with first-lien rates above 3.5%, meaning the potential exists for continued growth in that segment – which has been driving the majority of refinance activity for months now. Plus, more than 70% of tappable equity is held by borrowers with credit scores of 760 or higher, which creates opportunities for lower-risk cash-out lending products, even as rates rise. Though almost all recent cash-outs have resulted in rate reductions, in late 2018—when 30-year rates were close to 5%—more than 70% of cash-out borrowers accepted rate increases to access the equity in their homes. It would not be surprising to see similar behavior among ‘equity-centric’ borrowers as we move forward into 2022.”

To view the report in its entirety, click here.