DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

HUD began its Distressed Asset Stabilization Program (DASP) in 2010 in response to the massive amount of foreclosures brought on by the crisis as a way to sell those distressed or nonperforming loans to investors.

HUD began its Distressed Asset Stabilization Program (DASP) in 2010 in response to the massive amount of foreclosures brought on by the crisis as a way to sell those distressed or nonperforming loans to investors.

Critics of DASP claim that HUD should sell more of these distressed or nonperforming loans to nonprofits rather than profit-seeking investors. However, researchers from the Urban Institute concluded that all parties—HUD, the borrowers, and investors—stand to benefit when distressed loans are sold through DASP in a paper titled Selling HUD’s Nonperforming Loans: A Win-Win for Borrowers, Investors, and HUD released Wednesday.

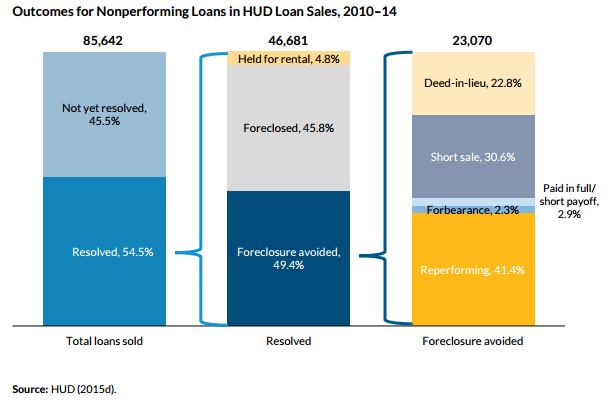

The loans sold through DASP are seriously delinquent and are likely to be foreclosed on without DASP's intervention, since servicers of loans in DASP pools are required to exhaust all loss mitigation possibilities. The goal of DASP is to maximize recoveries for the Federal Housing Administration, HUD’s parent agency, and help borrowers avoid foreclosure whenever possible. HUD has sold more than 100,000 distressed or nonperforming loans to private investors through DASP since the program’s inception in 2010.

The authors of the paper, Laurie Goodman (Director of Housing Finance Policy Center with Urban Institute) and Dan Magder (founder of Center Creek Capital Group), state that to properly evaluate DASP loan sales, one must keep in mind that DASP helps borrowers avoid foreclosure and encourages investors to pursue foreclosure alternatives, and that investors are able to better help borrowers than non-profits are.

“While nonprofits have a role in helping delinquent borrowers, their limited capital and capacity suggests that their ability to significantly increase their share of DASP loan purchases will be limited in the near-term,” the authors wrote.

Goodman and Magder concluded that critics of DASP calling for more participation from nonprofits in distressed loan sales are misguided, because “we question whether nonprofits have or can quickly build the capacity to service a significantly larger portion of the HUD portfolio than they are currently servicing—especially if they are working alone, and not in partnership with for-profit investors who have the capacity to conduct servicing at scale.”

Critics of DASP also hold what the authors say are misconceptions that the purchasers of these nonperforming loans often quickly push borrowers to foreclosure and that HUD is facilitating a “massive wealth transfer” from distressed borrowers to investors. Goodman and Magder say that while current servicing is not perfect and there have been servicing abuses, the aggregate data shows that loan sales through DASP produce far better outcomes for borrowers than foreclosure when DASP is not present.

Critics of DASP also hold what the authors say are misconceptions that the purchasers of these nonperforming loans often quickly push borrowers to foreclosure and that HUD is facilitating a “massive wealth transfer” from distressed borrowers to investors. Goodman and Magder say that while current servicing is not perfect and there have been servicing abuses, the aggregate data shows that loan sales through DASP produce far better outcomes for borrowers than foreclosure when DASP is not present.

Since DASP is not perfect, some changes are needed, according to Goodman and Magder. Among the changes they recommend are a refinement to the program to ensure that investors do not walk away from the most distressed properties, which makes it more burdensome for neighbors and more costly for municipalities who have to foot the bill. The authors also said they support increasing partnerships between investors and nonprofits to ensure the best outcomes for borrowers. Also, they encourage more transparency from HUD with regard to data and foreclosure alternatives.

“Better disclosure will not only help all parties more accurately evaluate the impact of the program, but should also pressure servicers who are less borrower-friendly,” the authors wrote.

Click here to view the complete paper.

Click here for more on HUD’s Distressed Asset Stabilization Program.