DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Underappraisals spiked to 15% in 2021 and 12% in 2022, when home prices experienced rapid growth, according to the Federal Housing Finance Agency (FHFA), while house price growth and underappraisal rates returned to more typical levels in early 2023.

As 2024 is predicted to see some similarities to 2023's chaotic market, home purchases remain complicated for many due to appraisals that come in below the homebuyer’s contract price offer.

From 2013–2020, the annual rate of appraisals below the contract price ranged from 7 to 9% of transactions. Low appraisals can also impact refinance borrowers by leading to less attractive loan terms, limiting borrowing amounts, or resulting in canceled transactions. Appraisers can consider price changes that have occurred since the time the comparables were sold and make adjustments known as market conditions adjustments or time adjustments.

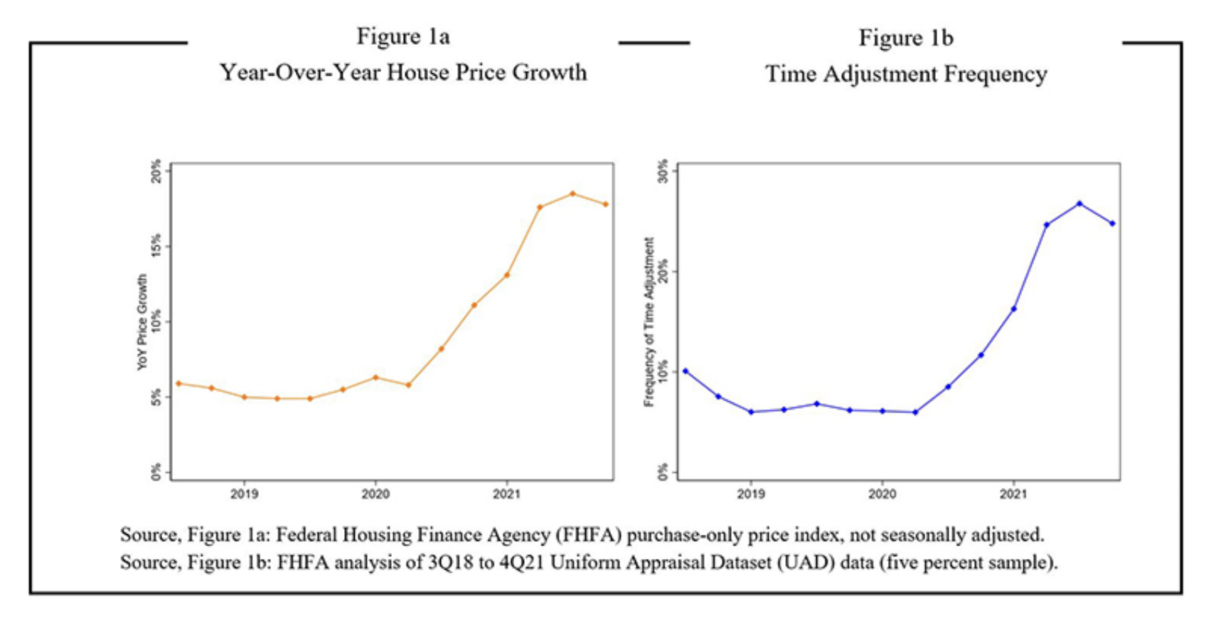

National Trends in Time Adjustment

During the analysis period, from Q3 of 2018 through Q4 of 2021, home prices generally rose, especially in 2021. National house prices grew annually from 5 to 18% over this period. For residential real estate, recent sales of comparable properties are commonly used to determine a property’s valuation.

Because comparable sales in this analysis are typically six months old at the time of the appraisal, expected time adjustments would range from approximately 2.5 to 9% of the sales price on average. However, time adjustments are not very common. During much of the analysis period, appraisers time-adjusted fewer than 10% of comparable sales. Even during the rapid price increases of 2021, time adjustment frequency rose only to about 25%.

While adjustments are not necessarily expected in every case, these rates seem to be considerably lower than local price growth would warrant.

Appraisers and Time Adjustments: When Are They Necessary?

When comparable sales are recent or home price growth is slow or flat, there may be no need for a time adjustment. Appraisers adjusted only about 5% of these properties, perhaps because these adjustments are too small to have much impact.

In conclusion, adjustments were unnecessary for, at most, 36% of properties where the predicted adjustment was between -1 and 2%. This result implies that appraisers should have time-adjusted 64% of comparables, far greater than the 13% adjusted.

Are Time Adjustments Accurate?

For predicted adjustments from 1 to 3%, actual time adjustments are within a few tenths of a percentage point. However, as the expected adjustment gets larger, the discrepancy grows. When the predicted adjustment is 5%, actual adjustments average 3%. At 10%, actual adjustments average 5%.

The report concluded that appraisers underutilize and underestimate time adjustments but do not attempt to determine the cause or propose potential solutions. One potential reason for underutilization is that these adjustments are some of the more analytically complex calculations appraisers might perform.

To read the full report, including more data, charts, and methodology, click here.