DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

According to a new Fannie Mae Perspectives Blog post written by Kevin Tillmann, Market Research Senior Associate for the National Housing Survey, and Steve Deggendorf, Senior Director of Market Research, consumers’ homeownership aspirations remain high despite higher home prices and the possibility of future interest rate hikes.

According to a new Fannie Mae Perspectives Blog post written by Kevin Tillmann, Market Research Senior Associate for the National Housing Survey, and Steve Deggendorf, Senior Director of Market Research, consumers’ homeownership aspirations remain high despite higher home prices and the possibility of future interest rate hikes.

According to the authors, “living the good life” is a subjective sentiment that can vary widely from household to household as many priortize financial security, their health, location, work-life balance or meaningful personal relationships.

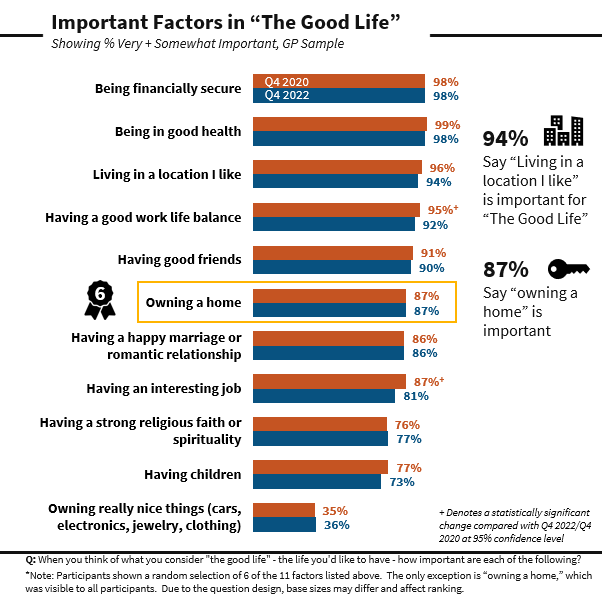

In the fourth quarter of 2020, Fannie Mae's Economic & Strategic Research (ESR) Group asked consumers which factors are most important to them as they consider "the good life" – defined by the survey as the "life they'd like to have." All but one of the eleven listed factors were very important to a large majority of people across all demographic groups. Now, more than two years later, Fannie Mae has reissued the survey to see what have changed following the COVID-19 pandemic, domestic and international unrest and war, and significant increases in home prices and interest rates.

Fannie Mae and the authors, to their surprise, found that consumers’ sense of “living the good life” has remained largely unchanged over the last two years; although there is more nuance when examining the data across race, age, income, and homeownership status.

Once again, financial security and good health remains at the top of the “good life” list. Eighty-seven percent of respondents indicated that owning a home remains very important, but all-in-all it ranked six out of the eleven possible options—roughly the same as having a good social circle (90%) or having a happy marriage or romantic relationships (86%). Additionally, more than twice as many consumers consider owning a home to be important compared to "owning really nice things," such as cars, electronics, jewelry, or clothing (36%).

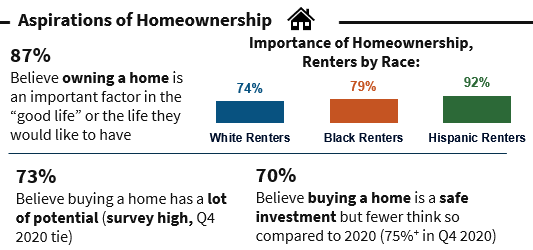

Looking more closely at the data across racial and homeownership status lines, a greater share of Hispanic renters (92%) consider homeownership to be important than Black renters (79%) and White renters (74%).

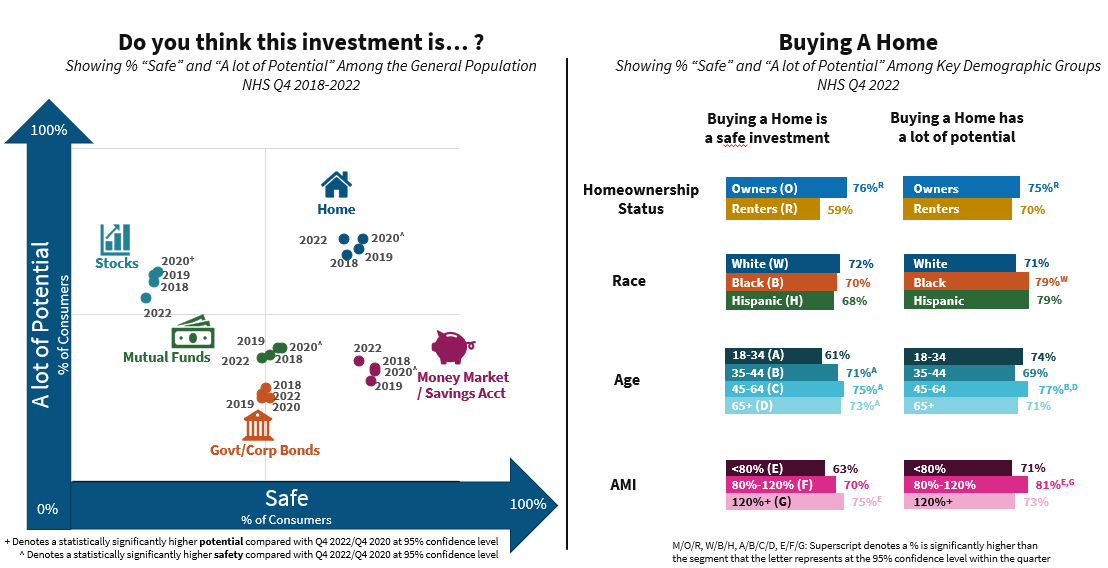

In addition, the survey asked consumers to consider the financial and non-financial benefits derived from either owning or renting. Respondents overwhelmingly indicated that owning a home was preferable to renting in every aspect listed.

In fact, associating homeownership with "having less stress" was one of the biggest shifts between the two most recent data sets. It was particularly true among renters (60% in 2022 compared to 40% in 2020). One possible reason is that many renters have seen their rents increase significantly while home affordability declined. Another is that homeownership may be perceived as offering greater privacy and security than renting, a lifestyle benefit that may have proved especially desirable three years into a pandemic.

“In 2022, 88% of Black consumers viewed 'living in a place where you and your family feel safe' as a benefit of homeownership, significantly higher than two years ago (72%),” the authors wrote. “For context, the percentage of the general population that listed that particular benefit also rose over the two-year period, but slightly less (from 83% to 88%).”

As Fannie Mae is still predicting recession conditions to occur in 2023, the resiliency of consumers' perceptions of homeownership relative to other investment options is noteworthy, especially during the previous three-year period of significant economic uncertainty. The survey data shows that consumers see homeownership as helping to deliver on a sense of financial security, which was also tied as the primary factor associated with the "good life." In fact, homeownership has strongly persisted as a perceived leading source of financial benefits dating all the way back to 2010, when Fannie Mae began the National Housing Survey.

“Given the consistency of our survey results, we expect consumers' longstanding and highly favorable attitude toward homeownership as an investment option will continue to persist, even in the face of possible recession,” the authors concluded. “Finally, in further support of homeownership's enduring appeal, our data showed clear non-financial benefits to owning a home, as well, that we believe provide additional dimensions of value for consumers that, for the most part, other financial assets do not confer.”

Click here to view the blog post in its entirety.