DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Risk of default among mortgage borrowers is on the rise, especially on loans being written right now, according to data from University Financial Associates.

Risk of default among mortgage borrowers is on the rise, especially on loans being written right now, according to data from University Financial Associates.

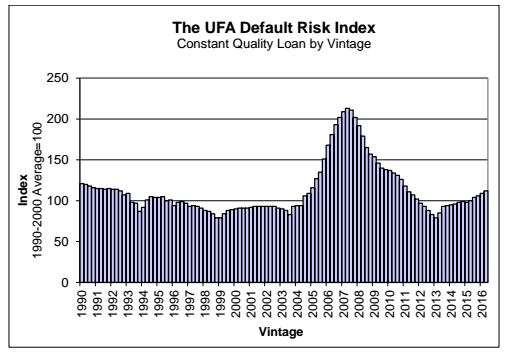

UFA’s latest default risk index for Q2, which measures the risk of default on newly originated prime and nonprime mortgages, ended at 112, up from Q1’s 109.

“Under current economic conditions, investors and lenders should expect defaults on loans currently being originated to be 12 percent higher than the average of similar loans originated in the 1990s,” the report stated.

That comparison is significant when looking at UFA’s graph of default risk since 1990, and seeing that the trends of the past four years closely resemble those between 1990 and 1994.

The takeaway for investors and lenders, according to Dennis Capozza, founding principal at UFA, is that there is a continuing upward trend in the risk of default for both prime and nonprime mortgage loans. While low unemployment rates are benefiting the mortgage market and low interest rates are fueling a buying spree, the lending risks in newly originated mortgages are increasing along with the maturity of the economic cycle.

“Mortgage risks are continuing to increase as this economic cycle matures,” Capozza said. “Consumer loan growth is at a seven-year high, and low mortgage interest rates are fueling a buying spree. The Federal Reserve is once again threatening to move interest rates higher.”

“Mortgage risks are continuing to increase as this economic cycle matures,” Capozza said. “Consumer loan growth is at a seven-year high, and low mortgage interest rates are fueling a buying spree. The Federal Reserve is once again threatening to move interest rates higher.”

Capozza said he expects the Fed will move cautiously in an election year, but added “Nevertheless, any increase in interest rates will raise the life-of-loan default risks for new originations.”

A number of factors affect the expected defaults on a constant-quality loan, UFA stated. Most important are worsening economic conditions. A recession causes an erosion of both borrower and collateral performance.

“Borrowers are more likely to be subjected to a financial shock, such as unemployment, and if shocked, will be less able to withstand the shock. Fed easing of interest rates has the opposite effect,” the report stated.