DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

While homebuyer confidence has continually fluctuated due to evolving economic conditions, the Fannie Mae Home Purchase Sentiment Index (HPSI) remained mostly flat in June, increasing by only 0.4 points to 66.0, as difficult supply and affordability conditions continue to weigh on the housing market.

While most of the HPSI’s six components were little changed month over month, survey respondents did report that homebuying conditions improved slightly in June compared to May. Even so, a significant majority of consumers continue to report that it’s a “bad time to buy” a home, as they have since mid-2021. The full index is up 1.2 points year-over-year.

“Confidence in the housing market appears to have plateaued at a relatively low level, suggesting that many consumers may be coming to terms with elevated mortgage rates and high home prices,” said Doug Duncan, Fannie Mae Senior VP and Chief Economist. “Home prices continue to be supported by the tight supply of homes available for sale, and, compared to the end of last year, fewer respondents today believe home prices will decrease over the next 12 months. Additionally, consumers’ mortgage rate expectations have tempered: A larger share of respondents think mortgage rates will stay the same over the next year, whereas mid-to-late last year, most thought rates would continue going up. This seems to signal that consumers are adapting to the idea that higher mortgage rates will likely stick around for the foreseeable future. We continue to forecast home sales to slow in the second half of the year, compared to the first half, due to ongoing affordability constraints and lack of housing supply.”

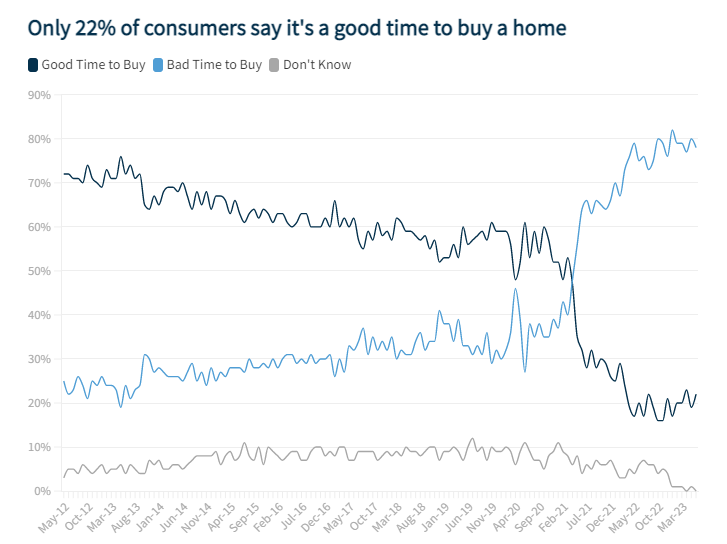

Home Purchase Sentiment Index Highlights

Fannie Mae’s Home Purchase Sentiment Index (HPSI) increased in June by 0.4 points to 66.0. The HPSI is up 1.2 points compared to the same time last year.

- Good/Bad Time to Buy: The percentage of respondents who say it is a good time to buy a home increased from 19% to 22%, while the percentage who say it is a bad time to buy decreased from 80% to 78%. As a result, the net share of those who say it is a good time to buy increased 5 percentage points month over month.

- Good/Bad Time to Sell: The percentage of respondents who say it is a good time to sell a home decreased from 65% to 64%, while the percentage who say it’s a bad time to sell increased from 34% to 36%. As a result, the net share of those who say it is a good time to sell decreased 3 percentage points month over month.

- Home Price Expectations: The percentage of respondents who say home prices will go up in the next 12 months decreased from 39% to 36%, while the percentage who say home prices will go down decreased from 28% to 26%. The share who think home prices will stay the same increased from 33% to 37%. As a result, the net share of those who say home prices will go up in the next 12 months remained unchanged month over month.

- Mortgage Rate Expectations: The percentage of respondents who say mortgage rates will go down in the next 12 months decreased from 19% to 16%, while the percentage who expect mortgage rates to go up decreased from 50% to 47%. The share who think mortgage rates will stay the same increased from 31% to 36%. As a result, the net share of those who say mortgage rates will go down over the next 12 months decreased 1 percentage point month over month.

- Job Loss Concern: The percentage of respondents who say they are not concerned about losing their job in the next 12 months remained unchanged at 77%, while the percentage who say they are concerned remained unchanged at 22%. As a result, the net share of those who say they are not concerned about losing their job decreased 1 percentage point month over month.

- Household Income: The percentage of respondents who say their household income is significantly higher than it was 12 months ago decreased from 20% to 19%, while the percentage who say their household income is significantly lower decreased from 12% to 10%. The percentage who say their household income is about the same increased from 67% to 71%. As a result, the net share of those who say their household income is significantly higher than it was 12 months ago increased 1 percentage point month over month.

To read the full report, click here.