DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

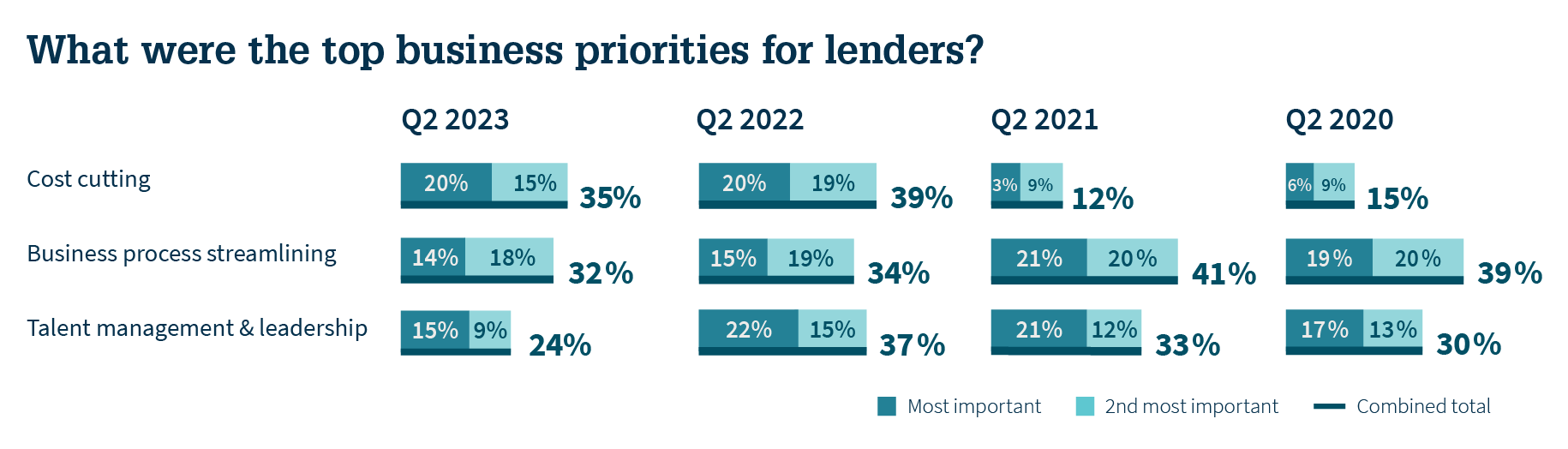

According to a new Fannie Mae Perspectives Blog authored by Doug Duncan, the SVP and Chief Economist for Fannie Mae, the most recent Mortgage Lender Sentiment Survey found that mortgage lending firms are again prioritizing cutting costs for the second year in a row as lender sentiments of the economy remained extremely pessimistic, continuing a trend that began in the third quarter of 2021.

According to a new Fannie Mae Perspectives Blog authored by Doug Duncan, the SVP and Chief Economist for Fannie Mae, the most recent Mortgage Lender Sentiment Survey found that mortgage lending firms are again prioritizing cutting costs for the second year in a row as lender sentiments of the economy remained extremely pessimistic, continuing a trend that began in the third quarter of 2021.

The survey, which reaches 232 lending institutions and highly placed senior mortgage executives, is meant to understand lenders’ top business priorities for the year and how they differ from previous surveys. Something new for this survey was the addition of questions to gauge lenders’ views about the U.S. economy and possible risk factors for the 2023 mortgage business.

Since the housing boom that started during the pandemic, the mortgage industry has faced a litany of challenges including high home prices, multiple and significant interest rate hikes, elevated inflation, tight inventory of homes for sale, and a global slowdown of economic growth.

According to the survey, the consensus among survey respondents is that both purchase and refinance origination activity will continue to slow throughout the remainder of the year.

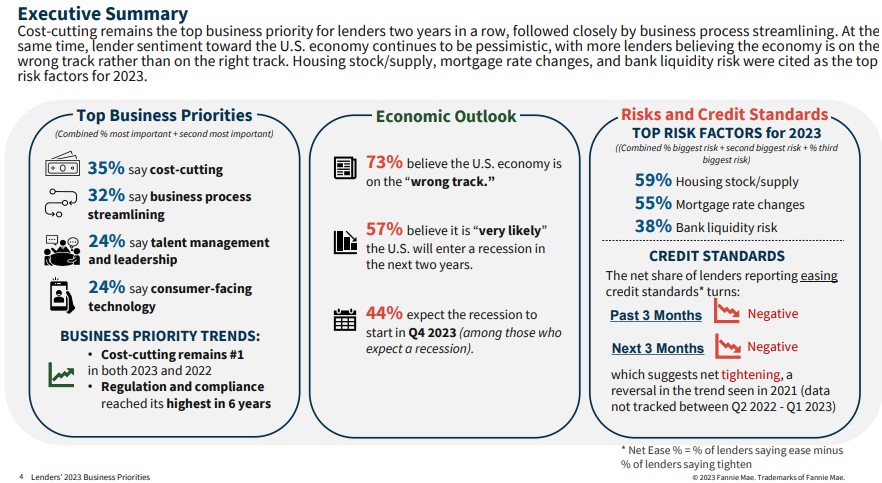

"For two consecutive years lenders have cited ‘cost-cutting’ as their top business priority. Investment in ‘business process streamlining’ has remained among the top three priorities since 2017. The importance of ‘talent management and leadership’ fell after peaking in 2022 but remained in third place, tied with ‘consumer-facing technology.’” Duncan wrote. “Notably ‘regulation and compliance’ reached its highest share in six years (since 2018), suggesting lenders are facing increased regulatory pressures.”

“A further examination of business priorities across the three institution types (depository institutions excluding credit unions, mortgage banks, and credit unions) yielded significant differences,” Duncan continued. “While cost-cutting, business process streamlining, and new products/services are mortgage banks' top business priorities, talent management, regulation/compliance, and business process streamlining are depository institutions' top focus. In other words, mortgage bank priorities reflect higher cost and revenue pressures, whereas depository institution priorities reflect the challenges of meeting regulatory changes and recruiting talent to drive sales. Lenders also pointed out the importance of having the right leadership team to coach and motivate staff in today's tough business environment.”

Seventy-three percent of respondents believe the U.S. Economy is on the “wrong track.” Notably, the vast majority of lenders (93%) believe the U.S. economy is "very likely" or "somewhat likely" to enter a recession in the next two years (57% and 37%, respectively). Among them, many (68%) expect the recession to start in Q3 or Q4 of this year (24 percent saying Q3 2023 and 44 percent saying Q4 2023). A comparison between institution types shows that depository institutions are more pessimistic than mortgage banks: They are both more likely than mortgage banks to believe that the economy is on the wrong track (82% vs. 66%) and to believe that the U.S. economy will "very likely" enter a recession in the next two years (65% vs. 48%).

Lenders were also asked about risk factors that could impact their bottom line this year: housing stock and supply and mortgage rates changes were cited as the biggest risk factors, followed by bank liquidity risk. Lenders were less concerned about cybersecurity, consumer access to credit, mortgage delinquencies, and the costs of goods and services.

“Regarding the impact of the recent banking turmoil (including lack of consumer confidence in banks and fears of bank collapse) on lenders' business operations or mortgage production or servicing, the magnitude of expected impact appears to be limited,” Duncan wrote. “Only about a third of lenders surveyed indicated that that they expected their business to be impacted. Some lenders commented that, with deposit outflows and cost of funds increasing, liquidity has been reduced, particularly for loans on portfolio. Likely due to the lack of capital and liquidity, compared to the 2021 results, significantly more lenders in this quarter's survey reported credit tightening than easing.”

“Overall, lenders' pessimistic sentiment toward the economy and their top risk concerns were reflected in this year's business priorities: cost-cutting and business process streamlining. Loan origination has yielded a loss since Q2 2022, and the average production cost per loan reached a new high in the first quarter at over $13,000 per loan.”

“Comparing institution types, the survey results also suggest differentiated business priorities. Depository institutions are more focused on talent management and compliance, while mortgage banks are putting more effort toward cost-cutting and new products/services for additional revenue streams.” Duncan concluded. “As always, lenders are adapting their strategies, depending on their business model, to remain competitive—and in today's business environment, this is likely much more challenging than previous years.”

Click here to view the study in its entirety.