DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

The U.S. Government Accountability Office (GAO) has issued a report on the Federal Emergency Management Agency (FEMA's) National Flood Insurance Program (NFIP), examining several objectives, including the actuarial soundness of Risk Rating 2.0; how premiums are changing; efforts to address affordability for policyholders; options for addressing the debt; and implications for the private market.

The U.S. Government Accountability Office (GAO) has issued a report on the Federal Emergency Management Agency (FEMA's) National Flood Insurance Program (NFIP), examining several objectives, including the actuarial soundness of Risk Rating 2.0; how premiums are changing; efforts to address affordability for policyholders; options for addressing the debt; and implications for the private market.

In analyzing the data, GAO reviewed FEMA documentation and analyzed NFIP, Census Bureau, and private flood insurance information. GAO also interviewed FEMA officials, actuarial organizations, private flood insurers, and insurance agent associations in its research.

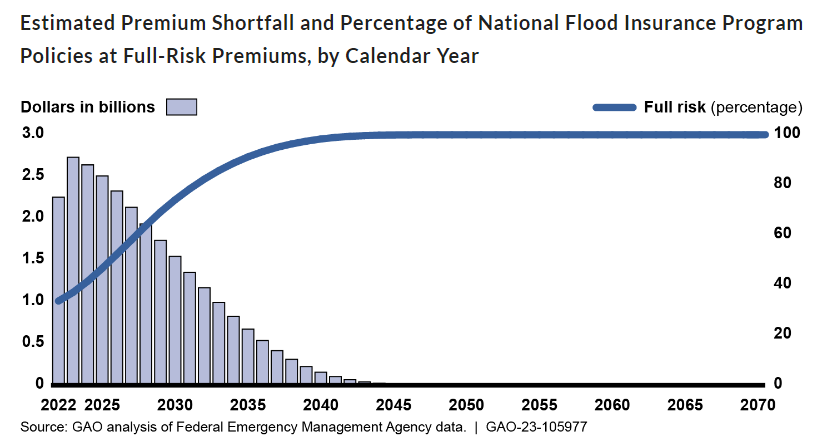

Through the NFIP, FEMA is charged with keeping flood insurance affordable and remaining financially solvent, but a historical focus on affordability has led to insurance premiums being lower than they should be. The NFIP hasn't collected enough revenue to pay claims, and has had to borrow billions from the U.S. Department of the Treasury.

In 2021, FEMA revamped how it sets premiums—more closely aligning them with the flood risk of individual properties through the implementation of Risk Rating 2.0, but affordability concerns accompany the premium increases some will experience. Risk Rating 2.0 aligns premiums with the flood risk of individual properties, but some other aspects of NFIP still limit actuarial soundness.

“For example, in addition to the premium, policyholders pay two charges that are not risk based,” said the report. “Unless Congress authorizes FEMA to align these charges with a property’s risk, the total amounts paid by policyholders may not be actuarially justified, and some policyholders could be over- or underpaying. Further, Congress does not have certain information on the actuarial soundness of NFIP, such as the risk that the new premiums are designed to cover and projections of fiscal outlook under a variety of scenarios. By producing an annual actuarial report that includes these items, FEMA could improve understanding of Risk Rating 2.0 and facilitate congressional oversight of NFIP.”

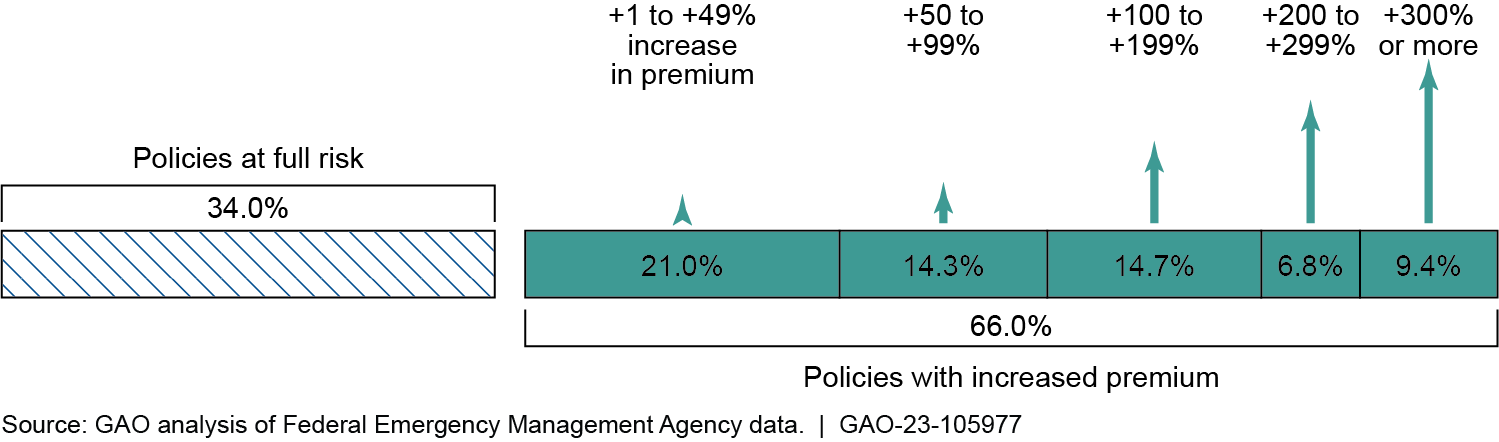

The launch of Risk Rating 2.0 has aligned premiums with risk, but affordability concerns accompany the premium increases. FEMA had been increasing premiums for a number of years prior to implementing Risk Rating 2.0. By December 2022, the median annual premium was $689, but this will need to increase to $1,288 in order to reach full risk. Under Risk Rating 2.0, approximately one-third of policyholders are already paying full-risk premiums. Many of these policyholders had their premiums reduced upon implementation of Risk Rating 2.0. All others will require higher premiums, including 9% who will eventually require increases of more than 300%. Gulf Coast states are reporting the largest premium increases, as policies in these states have been among the most underpriced, despite having some of the highest flood risks.

“We recommended that Congress consider creating a means-based assistance program that's reflected in the federal budget,” continued the GAO in its findings. “Risk Rating 2.0 does not yet appear to have significantly changed conditions in the private flood insurance market because NFIP premiums generally remain lower than what a private insurer would need to charge to be profitable. Further, certain program rules continue to impede private-market growth. Specifically, NFIP policyholders are discouraged from seeking private coverage because statute requires them to maintain continuous coverage with NFIP to have access to discounted premiums, and they do not receive refunds for early cancellations if they switch to a private policy. By authorizing FEMA to allow private coverage to satisfy NFIP’s continuous coverage requirements and to offer risk-based partial refunds for midterm cancellations replaced by private policies, Congress could promote private-market growth and help to expand consumer options.”

The GAO concluded that the following matters should be brought to Congress for consideration, specifically:

- Authorizing and requiring FEMA to replace two policyholder charges with risk-based premium charges

- Replacing discounted premiums with a means-based assistance program that is reflected in the federal budget

- Addressing NFIP’s current debt—for example, by canceling it or modifying repayment terms—and potential for future debt

- Authorizing and requiring FEMA to revise NFIP rules hindering the private market related to (1) continuous coverage and (2) partial refunds for midterm cancellations

Click here for more information on the GAO’s report FEMA's New Rate-Setting Methodology Improves Actuarial Soundness but Highlights Need for Broader Program Reform.