DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

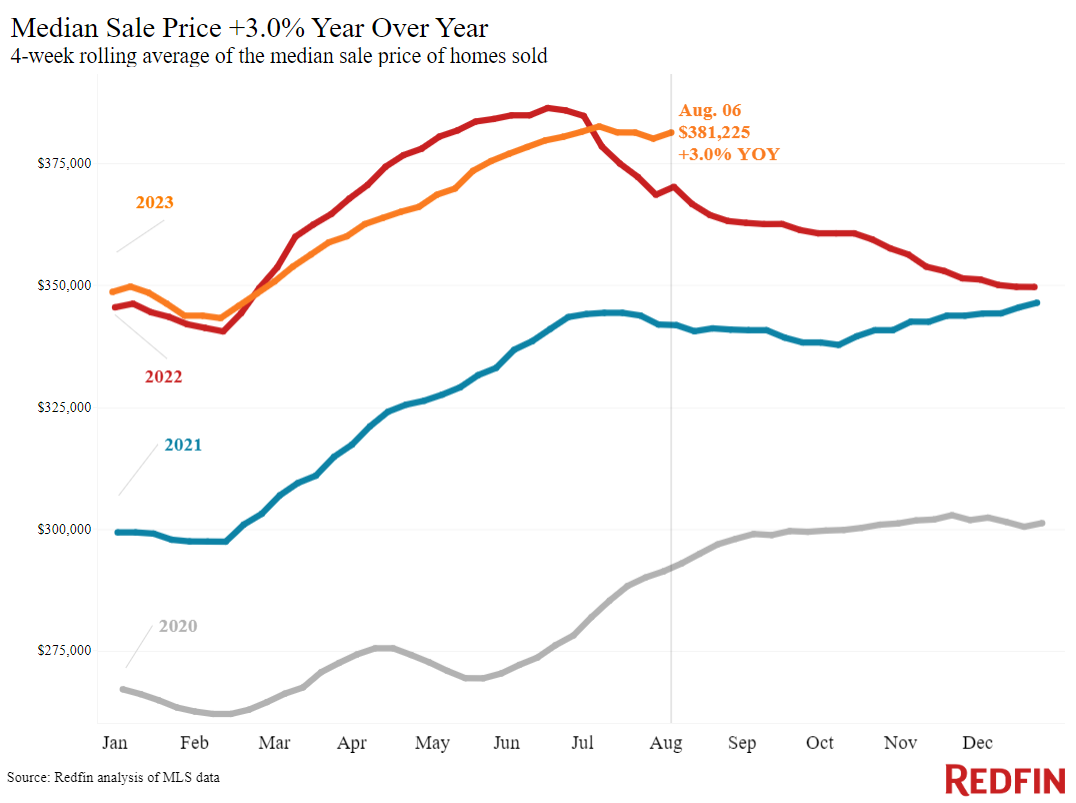

According to Redfin, the median home-sale price rose 3% year-over-year during the four weeks preceding Aug 6, the biggest increase since November.

However, prices are rising much more in certain parts of the country, such as Miami and Milwaukee, where double-digit increases were recorded.

According to Redfin, prices are increasing despite slow homebuying demand as buyers are still sidelined—or locked-out— of the market as rates are currently hovering around 7%; up from 3% in 2021 and an average 5.3% year-over-year. Redfin’s Homebuyer Demand Index, which measures early-stage demand through requests for tours and other buying services from Redfin agents, is down 5% from a year ago to its lowest level since March. Mortgage-purchase applications are down 27% from a year ago, also reaching their lowest level since March.

Further, limited inventory is pushing prices higher with so few homes on the market meaning there are now more house hunters than homes on the market in much of the country. The total number of homes for sale is down 18% year over year, the biggest drop since the start of 2022, and new listings are down 16%, with homeowners staying put to hold onto their relatively low mortgage rate. It’s worth noting that another reason prices are up on an annual basis is that they were coming down from an all-time high at this time last year.

“There’s a fair amount of demand for lower-priced single-family homes, which in this area means around $400,000 and under,” said Spokane, WA Redfin Premier agent Brynn Rea. “Buyers are looking for a deal to make up for high mortgage rates. That means the few move-in ready, relatively affordable homes on the market are selling fast, sometimes with multiple offers. But today’s bidding wars usually involve two or three offers, as opposed to the five to 10 offers we were seeing a year and a half ago—and many higher-priced homes are sitting on the market because it’s hard to afford today’s monthly payments.”

Leading indicators of homebuying activity, as highlighted by Redfin for the top-50 metropolitan areas, include:

- The daily average 30-year fixed mortgage rate was 7.05% on August 9. For the week ending August 3, the average 30-year fixed mortgage rate was 6.9%, slightly higher than a week earlier but slightly lower than the half-year high hit three weeks earlier.

- Mortgage-purchase applications during the week ending August 4 declined 3% from a week earlier, seasonally adjusted. Purchase applications were down 27% from a year earlier.

- The seasonally adjusted Redfin Homebuyer Demand Index—a measure of requests for home tours and other homebuying services from Redfin agents—was down 6% from a month earlier to its lowest level since March. It was down 5% from a year earlier.

- Google searches for “homes for sale” were down roughly 8% from a month earlier during the week ending August 5, and down about 11% from a year earlier.

- Touring activity as of August 6 was up 7% from the start of the year, compared with a 5% decrease at the same time last year, according to home tour technology company ShowingTime.

- The median home sale price was $381,225, up 3% from a year earlier. That’s the biggest increase since November.

- Sale prices increased most in Miami (12.6% YoY), Milwaukee (12.1%), West Palm Beach, FL (9.2%), Cincinnati (8.9%) and San Diego (8.6%).

- Home-sale prices declined in 12 metros, with the biggest drops in Austin, TX (-10.6% YoY), San Francisco (-6.3%), Phoenix (-3.6%), Fort Worth, TX (-3%) and Las Vegas (-2.6%).

- The median asking price of newly listed homes was $386,748, up 2.5% from a year earlier.

- The monthly mortgage payment on the median-asking-price home was $2,602 at a 6.9% mortgage rate, the average for the week ending August 3. That’s down about 1% ($39) from the record high hit three weeks earlier, but up 18% from a year earlier.

- Pending home sales were down 13.2% year over year, continuing a 15-month streak of double-digit declines.

- Pending home sales fell in all but three of the metros Redfin analyzed. They declined most in Providence, RI (-28.9% YoY), Newark, NJ (-26.4%), Boston (-24.9%), Seattle (-24.5%) and Warren, MI (-24.3%). They increased 1.9% in Las Vegas, and roughly 1% in Austin, TX and West Palm Beach.

- New listings of homes for sale fell 16.5% year over year.

- New listings declined in all metros Redfin analyzed. They fell most in Las Vegas (-37.5% YoY), Phoenix (-33.1%), Chicago (-26.7%), Oakland, CA (-25.3%) and New Brunswick, NJ (-24.3%).

- Active listings (the number of homes listed for sale at any point during the period) dropped 17.9% from a year earlier, the biggest drop since February 2022. Active listings were essentially flat from a month earlier; typically, they post month-over-month increases at this time of year.

- Months of supply—a measure of the balance between supply and demand, calculated by the number of months it would take for the current inventory to sell at the current sales pace—was 2.7 months, roughly the same as a year earlier. Four to five months of supply is considered balanced, with a lower number indicating seller’s market conditions.

- 43.6% of homes that went under contract had an accepted offer within the first two weeks on the market, up from 41% a year earlier.

- Homes that sold were on the market for a median of 28 days, up from 24 days a year earlier.

- 35.3% of homes sold above their final list price, down from 42% a year earlier.

- On average, 6.1% of homes for sale each week had a price drop, down from 6.5% a year earlier.

- The average sale-to-list price ratio, which measures how close homes are selling to their final asking prices, was 99.9%. That’s down from 100.5% a year earlier.

Click here to view the report in its entirety.