DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

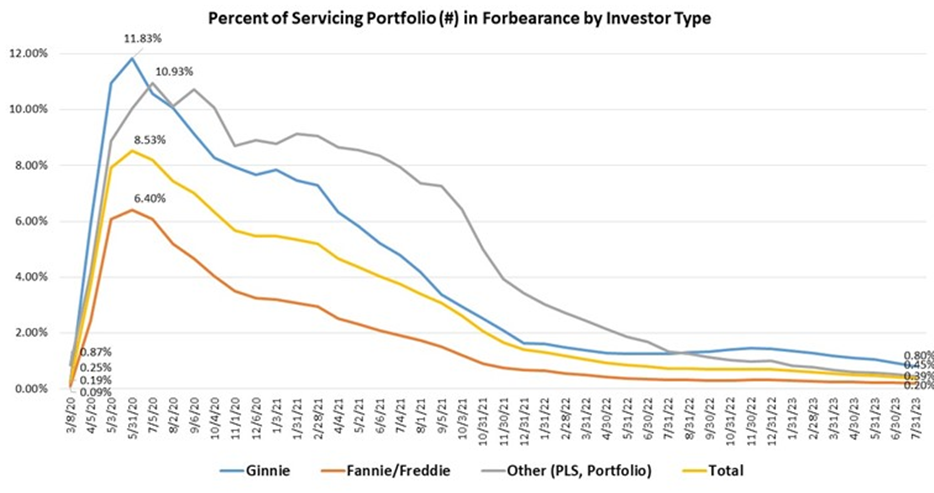

The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance dropped by five basis points from 0.44% of servicers’ portfolio volume in the prior month to 0.39% as of July 31, 2023. According to MBA’s estimate, 195,000 homeowners are now in forbearance plans. Since March 2020, mortgage servicers have provided forbearance to approximately 7.9 million borrowers nationwide.

The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance dropped by five basis points from 0.44% of servicers’ portfolio volume in the prior month to 0.39% as of July 31, 2023. According to MBA’s estimate, 195,000 homeowners are now in forbearance plans. Since March 2020, mortgage servicers have provided forbearance to approximately 7.9 million borrowers nationwide.

In July 2023, the share of Fannie Mae and Freddie Mac (GSE) loans in forbearance decreased just one basis point from 0.21% to 0.20%. Ginnie Mae loans in forbearance decreased 13 basis points from 0.93% to 0.80%, and the forbearance share for portfolio loans and private-label securities (PLS) decreased seven basis points from 0.52% to 0.45%.

“The prevalence of forbearance plans has dramatically dropped since 2020, and the reasons that borrowers are in forbearance are changing,” said Marina Walsh, CMB, MBA’s VP of Industry Analysis. “About two-thirds of borrowers are still in forbearance because of the effects of COVID-19, but a growing share of borrowers are in forbearance for other reasons that cause temporary hardship such as financial distress or natural disasters. With the COVID-19 national emergency lifted, Fannie Mae and Freddie Mac recently announced the retirement of certain COVID-19 flexibilities relating to forbearance plans and workouts.”

By reason, 69.3% of borrowers were reported in forbearance because of COVID-19. Another 6.5% were in forbearance due to a natural disaster. The remaining 24.2% of borrowers were in forbearance for other reasons, such as a temporary hardship caused by job loss, death, divorce, disability, etc.

Issued August 9, Lender Letter LL-2023-07 COVID-19 Payment Deferral and Fannie Mae Flex Modification for COVID-19 Impacted Borrowers updates policies previously published in LL 2021-07. Effective November 1, 2023, the Quality Right Party Contact (QRPC) flexibility will be removed when evaluating borrowers for a COVID-19 payment deferral or flex modification. Eligibility criteria for these options will be revised to facilitate their retirement, along with the announcement of a final evaluation date and modification effective date.

“Given the recent natural disasters impacting California, Washington, and Hawaii, forbearance is one way for mortgage servicers to mitigate the potential impacts on homeowners,” said Walsh.

CoreLogic estimates that approximately 3,088 single- and multifamily residential properties with a combined reconstruction value (RCV) of $1.3 billion were reported within three preliminary wildfire perimeters on Maui. FEMA has more than 600 personnel on the ground on Maui tasked with reaching survivors where they are, and residents now have the option to apply for federal disaster assistance at a joint Disaster Recovery Center recently opened at the University of Hawaii Maui College in Kahului, Hawaii.

By stage, 36.5% of total loans in forbearance were in the initial forbearance plan stage, while 53.3% were in a forbearance extension. The remaining 10.3% were forbearance re-entries, including re-entries with extensions.

Total completed loan workouts from 2020 and onward (repayment plans, loan deferrals/partial claims, loan modifications) that were current as a percent of total completed workouts decreased to 73.73% in July from 74.70% the previous month.

Of the cumulative forbearance exits for the period from July 1, 2020, through July 31, 2023, at the time of forbearance exit:

- 29.5% resulted in a loan deferral/partial claim.

- 17.8% represented borrowers who continued to make their monthly payments during their forbearance period.

- 18% represented borrowers who did not make all of their monthly payments and exited forbearance without a loss mitigation plan in place yet.

- 16.1% resulted in a loan modification or trial loan modification.

- 10.8% resulted in reinstatements, in which past-due amounts are paid back when exiting forbearance.

- 6.5% resulted in loans paid off through either a refinance or by selling the home.

- The remaining 1.2% resulted in repayment plans, short sales, deed-in-lieus or other reasons.

The five states with the highest share of loans that were current as a percent of servicing portfolio included:

- Washington

- Colorado

- Idaho

- Oregon

- California

The five states with the lowest share of loans that were current as a percent of servicing portfolio included:

- Louisiana

- Mississippi

- Indiana

- New York

- West Virginia