DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

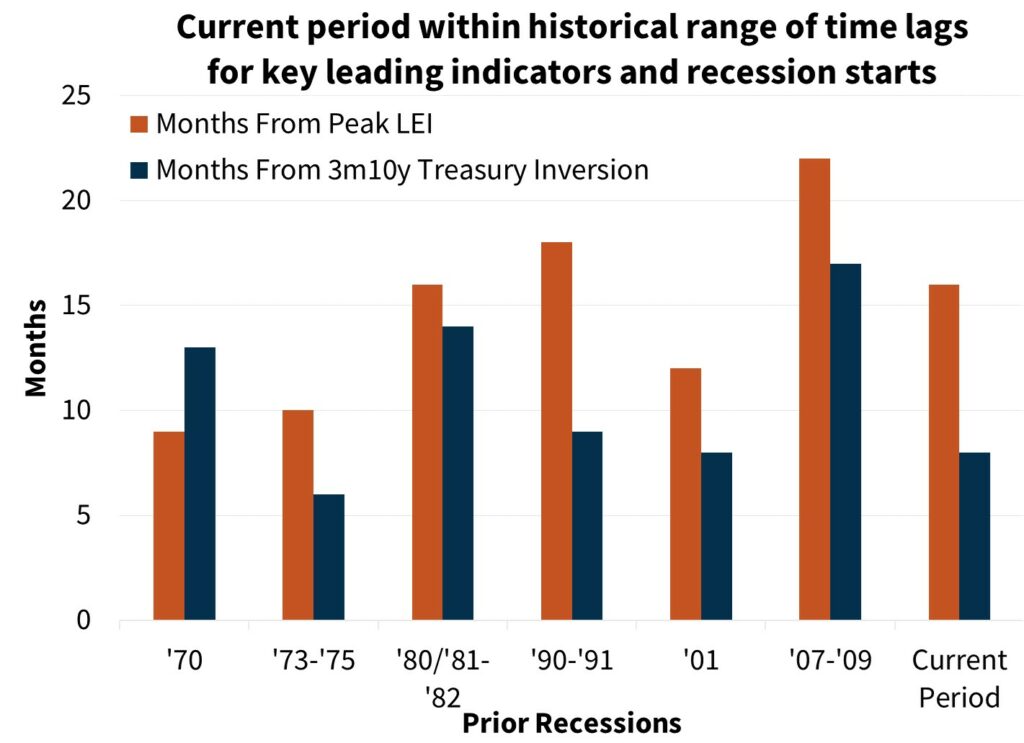

Fannie Mae has released a new analysis examining the likelihood of a 'soft landing' or a mild recession amid America's uncertain economic standing. Recent economic data has pointed to a stronger economy than previously expected, but the current business cycle contours still point to an eventual downturn, according to the August 2023 commentary from the Fannie Mae Economic and Strategic Research (ESR) Group.

Given the recent flurry of strong consumption data combined with two consecutive months of annualized Consumer Price Index (CPI) measures coming in close to the Fed’s 2% inflation target, the ESR Group notes that the odds of a “soft landing” have increased.

However, the full lagged effects of monetary policy tightening are still working their way through the economy, according to the ESR Group. Wage growth also likely remains too high to be consistent with 2 percent inflation over the long run, which the ESR Group believes will keep monetary policy tight.

Additionally, the ESR Group posits that the recent rise in medium- and longer-term Treasury yields will likely weigh on interest-rate-sensitive sectors in coming quarters. While the ESR Group notes that both the “if” and “when” of a recession are uncertain given the strength of recent economic data and decelerating inflation, their baseline forecast is for one to occur, now expected to begin in the first half of 2024.

Regardless of whether the economy enters a recession, the ESR Group forecasts home sales to remain subdued within a tight range. If the economy avoids a recession, the ESR Group expects home sales activity would continue to be suppressed by a lack of existing home inventory for sale combined with continued affordability constraints and homeowners remaining “locked in” to their low mortgage rate.

Alternatively, if the economy enters a recession, improvements in affordability and inventory stemming from likely lower interest rates are expected to be offset at least in part by a weaker labor market, tighter credit, and worsened consumer confidence. Regarding new homes, both sales and construction have performed comparatively well despite higher mortgage rates to date; however, the ESR Group notes some downside risk given mortgage rates are again near 7% and homebuilder confidence pulled back in August.

Interest Rates Moving Higher

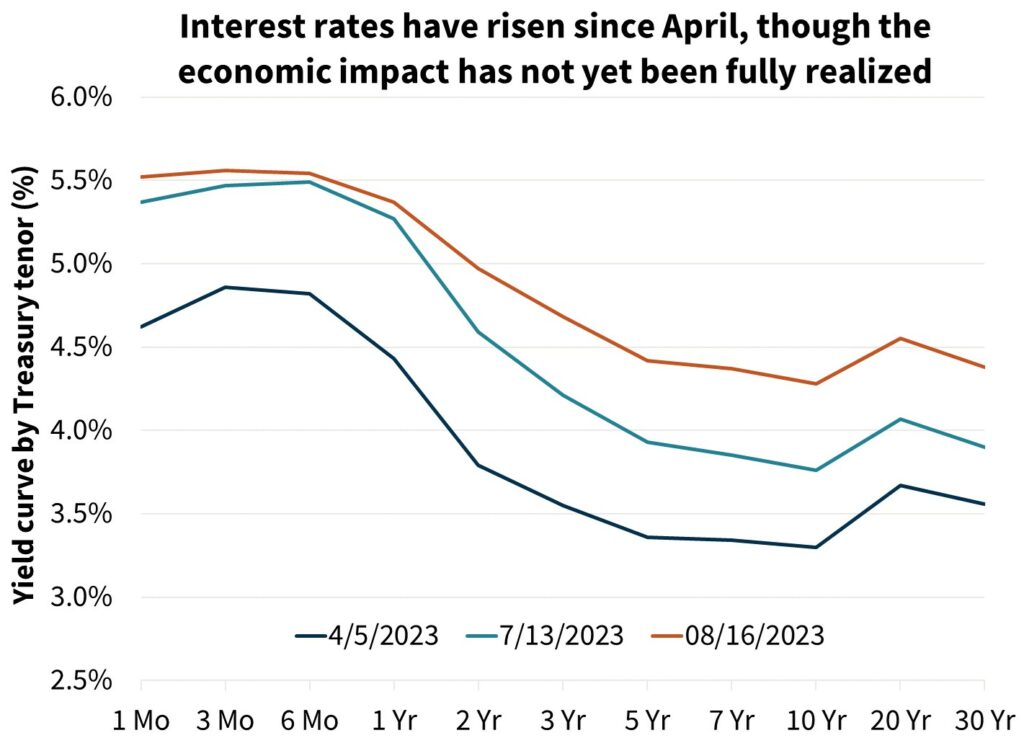

Fannie Mae experts expect that further fed funds rate hikes are off the table for now following the latest hike in July, given decelerating inflation measures and the lagged effects of tightening that has already occurred. However, the mid and longer end of the yield curve has moved up considerably in recent months following the decline in yields after the spring bank failures.

The two-year Treasury yield as of August 16th was hovering around 5%, while the 10-year yield closed at 4.28%, eclipsing the previous recent high in October of last year and hitting the highest point since late 2007.

The drivers of these recent rises are likely a mix of related factors such as:

- Strong economic data coupled with decelerating inflation is leading to financial markets pricing in fewer and less aggressive short-term rate cuts next year.

- Financial markets may be reconsidering what the long-run neutral real interest rate currently is. For the past 15 years of low growth and inflation it has been widely viewed that the neutral long-run fed funds rate was approximately 2.5% (with a 2% inflation target, this implies a 0.5% real rate). With growth now seemingly more robust despite higher rates, this suggests that the real neutral rate may be rising.

- Following the debt ceiling resolution, the Treasury is issuing a heightened level of debt while fiscal deficits are still large and rising. Markets may be now considering the need for higher longer run interest rates in order for that large of a Treasury issuance to be absorbed by market participants, especially in light of the Fed running off its balance sheet and foreign official buyers being less active than they have been in the past.

“It is easy to run your forecast ship aground by underestimating the American consumer,” said Doug Duncan, Senior VP and Chief Economist at Fannie Mae. “Despite reduced saving, increased rollover credit card balances, and rising credit costs, consumers are sustaining consumption, supported by a decline in inflation. Nonetheless, tightening monetary policy takes a toll. Will it result in a recession? Our base case forecast is a mild recession, and it looks as though the alternative is a soft landing, which is slow growth with only a small increase in unemployment. The difference between those two alternative outcomes is not expected to make much difference to home sales. The risk to housing activity is that inflation has bottomed out and begins to reaccelerate, requiring additional tightening from the Fed.”

To read the full report, including more data, charts, and methodology, click here.