DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

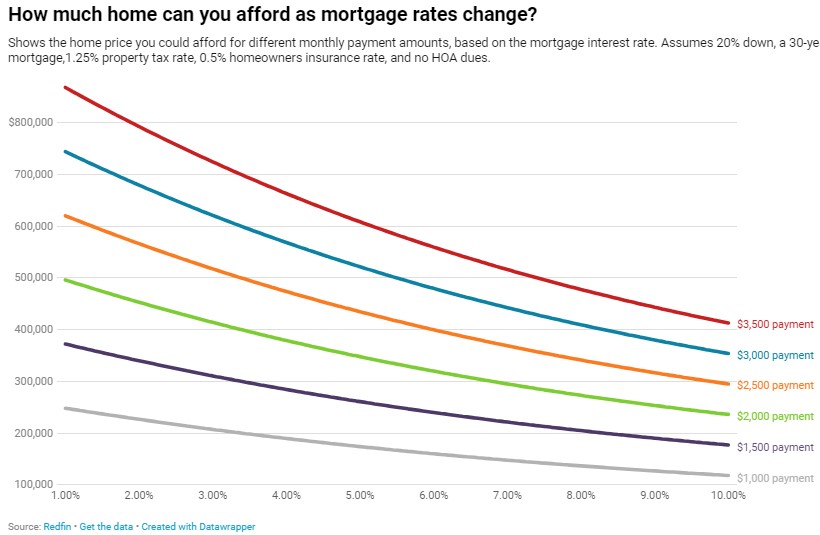

As mortgage rates hover around the 7% mark, these rates are cutting into buyers’ budgets according to a new report from Redfin which found that a buyer on a $3,000 monthly budget can afford a home valued at $429,000 assuming a 7.4% mortgage. Over the course of the last year, that buyer has last $71,000 in purchasing power year-over-year; that means last year they could have afforded a home valued at $500,000 at the then mortgage rate of 5.5%.

As mortgage rates hover around the 7% mark, these rates are cutting into buyers’ budgets according to a new report from Redfin which found that a buyer on a $3,000 monthly budget can afford a home valued at $429,000 assuming a 7.4% mortgage. Over the course of the last year, that buyer has last $71,000 in purchasing power year-over-year; that means last year they could have afforded a home valued at $500,000 at the then mortgage rate of 5.5%.

The daily average 30-year mortgage rate was 7.36% on August 23, down slightly from a peak the day before but still close to its highest level in more than 20 years. To look at affordability another way, the monthly mortgage payment on the typical U.S. home, which costs about $380,000, is roughly $2,700 with a 7.36% mortgage rate. The monthly payment would be $400 lower—around $2,300—with last year’s 5.5% rate.

This combination of high rates and low inventory have sidelined many would-be buyers. Home purchase applicaitions dropped to their lowest level in almost 30 years as of Aug. 18 and Redfin’s Homebuyer Demand Index, which measures requests for home tours and other services, was down 7% year-over-year.

“The buyers out there right now are the ones who need to move,” said Phoenix Redfin Premier agent Kim Lotz. “I’m working with one couple from out of state who are coming to Phoenix because of a job transfer; they don’t have the luxury of waiting for mortgage rates to come down.”

There’s more demand in some parts of the country than others. In Nashville, TN, for instance, Redfin Premier agent Kristin Sanchez says there are more buyers than sellers.

“Some buyers are hoping they can get a home for under asking price to make up for high interest rates because they’re hearing the housing market is slow. But what’s happening nationally isn’t necessarily true here,” Sanchez said. “Tennessee is a hot spot for people relocating from other states. There are plenty of jobs, and the area is starving for inventory. So despite high rates, there are more house hunters than houses for sale. Homes that are priced competitively and in good condition are typically selling at or just over asking price with two or three offers.”

Other leading indicators of homebuying activity, as highlighted by Redfin, include:

- The daily average 30-year fixed mortgage rate was 7.36% on August 23, near a two-decade high. For the week ending August 17, the average 30-year fixed mortgage rate was 7.09%, the highest level in more than 20 years.

- Mortgage-purchase applications during the week ending August 18 declined 5% from a week earlier, seasonally adjusted. Home-purchase applications dropped to their lowest level since 1995. Purchase applications were down 30% from a year earlier.

- The seasonally adjusted Redfin Homebuyer Demand Index was down about 2% from a month earlier. It was down 7% from a year earlier, the biggest decline since April.

- Google searches for “homes for sale” were down 7% from a month earlier during the week ending August 19, and down about 14% from a year earlier.

- Touring activity as of August 20 was up 2% from the start of the year, compared with a 6% decrease at the same time last year, according to home tour technology company ShowingTime.

Click here to see the report in its entirety.