DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Key Findings:

- Women have to save the longest to become a homeowner in Rhode Island, Kentucky and Hawaii.

- Women have the shortest savings period to become a homeowner in Vermont, West Virginia and Montana.

- Rhode Island, Kentucky and Oklahoma have the largest gender disparity in savings periods to become a homeowner.

- Vermont, Connecticut and California have the smallest gender disparity in savings it takes to buy a home.

However, overall, considering the expectations and financial pressures women are faced with, how much longer might it take for them to save enough for a home than it takes for men? This study combines U.S. Census income data with state-by-state real estate data to determine how long it takes women to afford a home in each state.

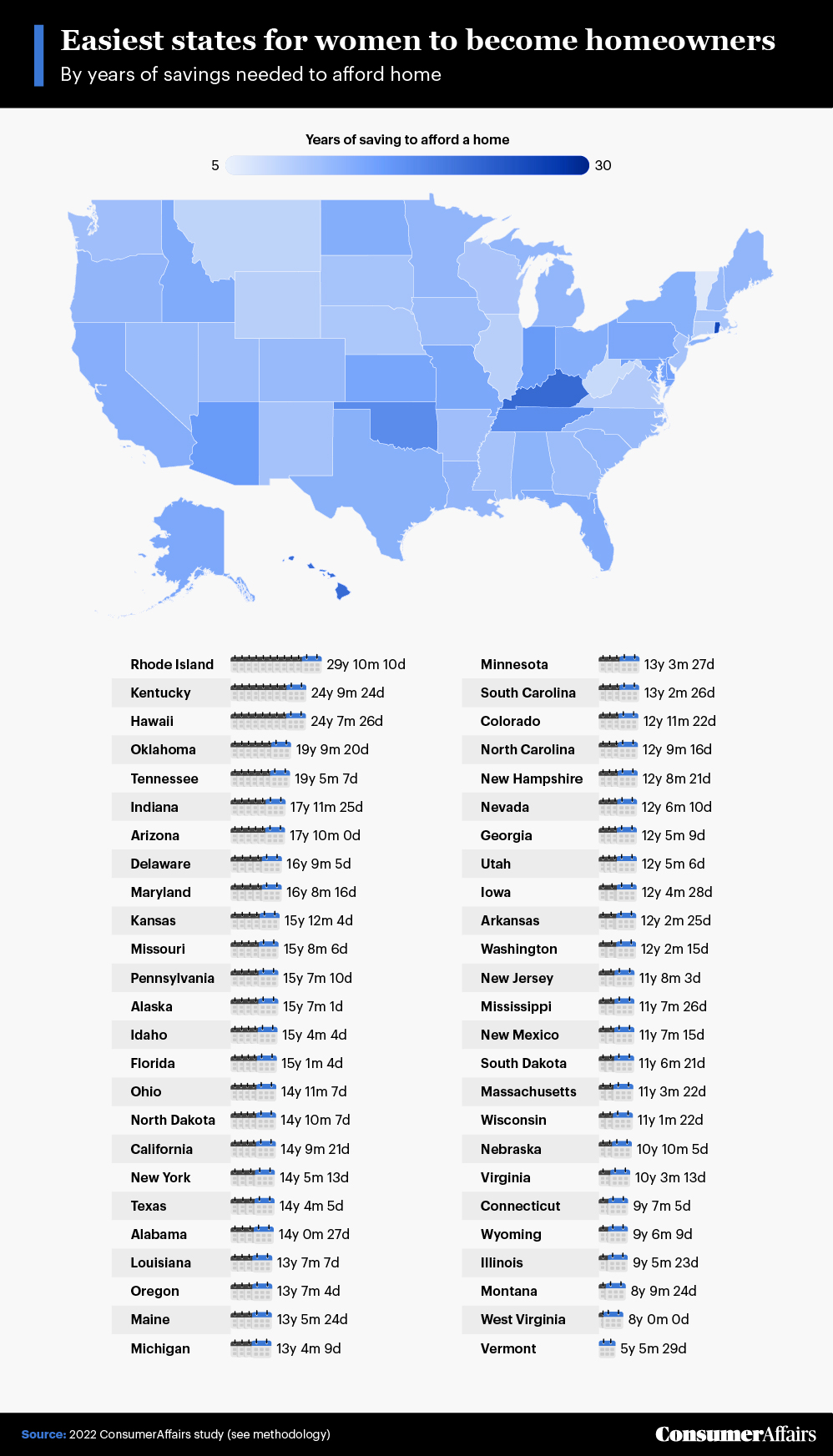

Saving up for real estate

To determine how long it takes women to save enough money for a home, ConsumerAffairs first looked at the median pay for women in each state along with the median down payment in each state.

The question remains, based on women’s income and the amount they might need to save for a down payment, how long would it take to have enough money to buy a home? To find out, ConsumerAffairs coupled the data above with the Americans’ average national savings percentages. The chart below shows how much estimated time it may take for a woman to save for a home in each state.

Vermont is the easiest place for a woman to afford buying a home, with the average woman needing to save for just five years, five months and 29 days for a down payment.

Women in Rhode Island likely have the hardest time: It could take them almost 30 years to buy a house. Although the median income of women in these two states is similar —$51,590 and $54,123, respectively—, as the median down payment for a house in Rhode Island is a whopping $58,621 higher than that in Vermont.

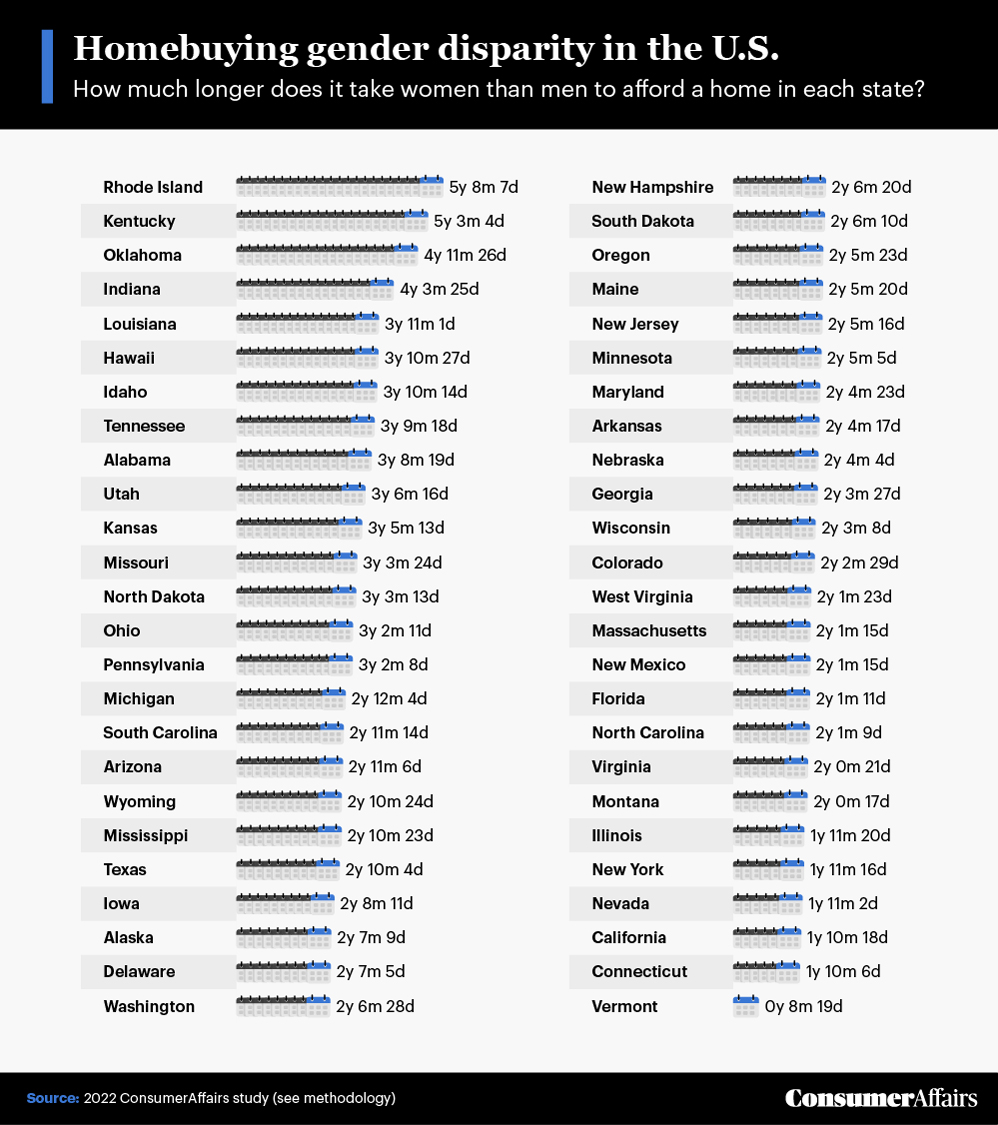

How much harder do women have it?

After determining how long it can take for women to afford homes, ConsumerAffairs compared their numbers to men’s. The graph below shows how much longer than the average man a woman would need to save to afford a home in each state.

Along with being the most challenging state for women to save for a down payment, Rhode Island also has the most significant gender disparity regarding the time needed to save for a home. A woman would have to save for nearly six years longer than her male counterpart to buy a home in the state.

Kentucky and Oklahoma also have significant gender gaps in homebuying: It can take women four to five years longer than men to save for a home in these states.

On the other hand, Vermont has the smallest gender gap: It could take just under nine months longer for a woman to afford a home there than it would for a man. Connecticut and California also have relatively low gender disparity, with women needing to save for less than two years longer than men to afford a home. The gender disparity in Nevada, New York and Illinois was almost equally low.

To read the full analysis, including more charts and methodology, click here.