DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

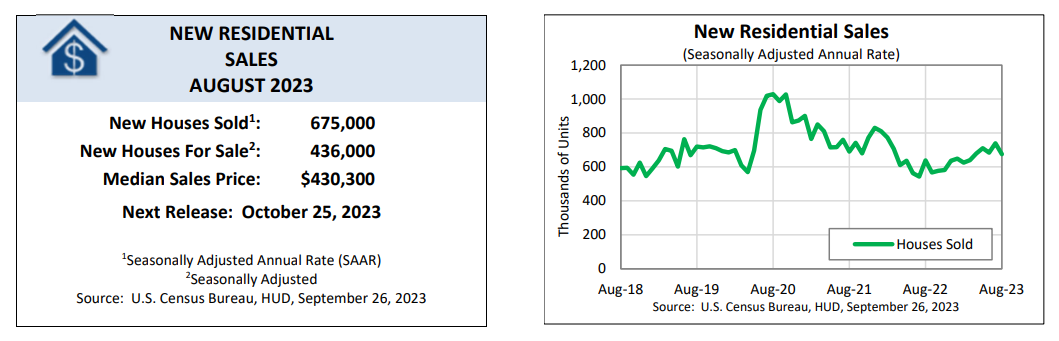

The U.S. Census Bureau and the U.S. Department of Housing and Urban Development (HUD) have released its new residential sales statistics for August 2023, finding that sales of new single‐family houses in August were at a seasonally adjusted annual rate of 675,000—8.7% below the revised July rate of 739,000, but 5.8% above the August 2022 estimate of 638,000.

The U.S. Census Bureau and the U.S. Department of Housing and Urban Development (HUD) have released its new residential sales statistics for August 2023, finding that sales of new single‐family houses in August were at a seasonally adjusted annual rate of 675,000—8.7% below the revised July rate of 739,000, but 5.8% above the August 2022 estimate of 638,000.

“New single-family home sales fell by 8.7% in August to a seasonally adjusted annualized rate (SAAR) of 675,000, but this followed a meaningful upward revision for the July figure of 25,000 to 739,000 SAAR units,” said Doug Duncan, Chief Economist at Fannie Mae.

HUD and the Census Bureau reported that the median sales price of new houses sold in August 2023 was $430,300, with the average sales price at $514,000.

In terms of for sale inventory and housing supply, the seasonally‐adjusted estimate of new homes for sale at the end of August was 436,000, representing a supply of 7.8 months at the current sales rate.

“July sales were the highest since February 2022. In terms of the supply of listings, the months’ supply jumped eight-tenths to 7.8, the highest since March,” added Duncan. “The supply of new homes for sale rose 1.2% to 436,000. Of note is that the inventory of completed homes for sale continued to climb and is now at the highest level since April 2020.”

The average mortgage rate in August sat above the 7% mark, thus adding another affordability hurdle in the quest for housing for the nation’s home seekers.

“August was the first month in which sales experienced mortgage rates near or above 7% since last November, which likely explains part of the decline,” added Duncan. “The drop was consistent with the recent decline in the homebuilders’ sentiment survey, as well–although some of this month’s sales drop may be give-back from the strong July reading. The July and August numbers are in line with our current outlook for Q3, though further increases in mortgage rates point to additional softening and pose downside risk to our outlook.”

Despite jobs in the construction sector jobs in the U.S. increasing by 212,000 (2.7%) on a year-over-year basis in August, the National Association of Home Builders (NAHB) reports builder confidence in the market for newly built single-family homes in September fell five points to 45, according to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI).

“High mortgage rates are clearly taking a toll on builder confidence and consumer demand, as a growing number of buyers are electing to defer a home purchase until long-term rates move lower,” said NAHB Chief Economist Robert Dietz. “Putting into place policies that will allow builders to increase the housing supply is the best remedy to ease the nation’s housing affordability crisis and curb shelter inflation. Shelter inflation posted a 7.3% year-over-year gain in August, compared to an overall 3.7% consumer inflation reading.”

First American Deputy Chief Economist Odeta Kushi added, “According to NAHB, 32% of builders reported cutting home prices in September, the largest share of builders cutting prices since December 2022, while 59% of builders provided sales incentives of all forms in September, more than any month since April 2023. Incentives can come in the form of rate buy-downs, paying points for buyers, offering price reductions, and offering upgrades on interior quality features. As a result of these incentives, the new-home market has fared significantly better than the existing home market, which continues to suffer from the mortgage rate lock-in effect. Builders are benefitting from the lack of re-sale inventory, but the increase in mortgage rates in August proved to be a significant headwind. Higher rates price out prospective buyers and, as a result, new home sales fell.”