DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

As the price of homes continues rising, down payment requirements have grown in direct proportion to home prices, and attaining a down payment is a crucial—and the most difficult—part of the homebuying process for most consumers.

The gold standard of down payments is 20% of the purchase price, but as that number has grown by 10’s of thousands in the last few years, more-and-more potential homebuyers are turning to family—mainly the Bank of Mom and Dad—to speed up the savings process to the tune of 2-in-5 (39%) homebuyers according to the latest LendingTree survey which reached just under 2,000 consumers.

Key finding from the report as highlighted by LendingTree include:

- Saving for a down payment can take years — but receiving help from the bank of Mom and Dad can speed up that process. 39% of homeowners have received down payment assistance, with help from parents leading the way. This is most common among younger Americans: 78% of Gen Z homeowners report some financial support for a down payment, mostly from their parents. In addition, 54% of millennials have received down payment help, followed by 33% of Gen Xers.

- The 20% down payment requirement is a common misconception among Americans. Almost a third (31%) of Americans think putting down 20% for a down payment is obligatory. However, 59% of current homeowners who have or have had a mortgage say their down payments were less than 20% of the home’s purchase price, and just 29% put down 20% or more. Older mortgage holders are more likely to pony up for their down payment, with 40% of these baby boomers putting down 20% or more.

- Some consumers, primarily older generations, enjoy the mortgage-free lifestyle. One in 10 Americans never took out a mortgage, while 15% had a mortgage but have since paid it off. Baby boomers are the most likely to have paid off their mortgages, at 29%. Meanwhile, the likelihood of never having a mortgage is relatively similar across generations.

- Most homeowners say they have a solid understanding of the mortgage process, but there’s still uncertainty. 43% of homeowners say they know a lot about the process of getting a mortgage, while another 12% claim to be experts. On the other hand, 11% admit they don’t know anything about getting a mortgage, despite being homeowners. When it comes to mortgage programs, conventional loans are the most widely used, with 60% of past or present mortgage holders saying they most recently used a conventional loan. Only 12% used a Federal Housing Administration (FHA) loan, while 6% each used jumbo loans and Department of Veterans Affairs (VA) loans.

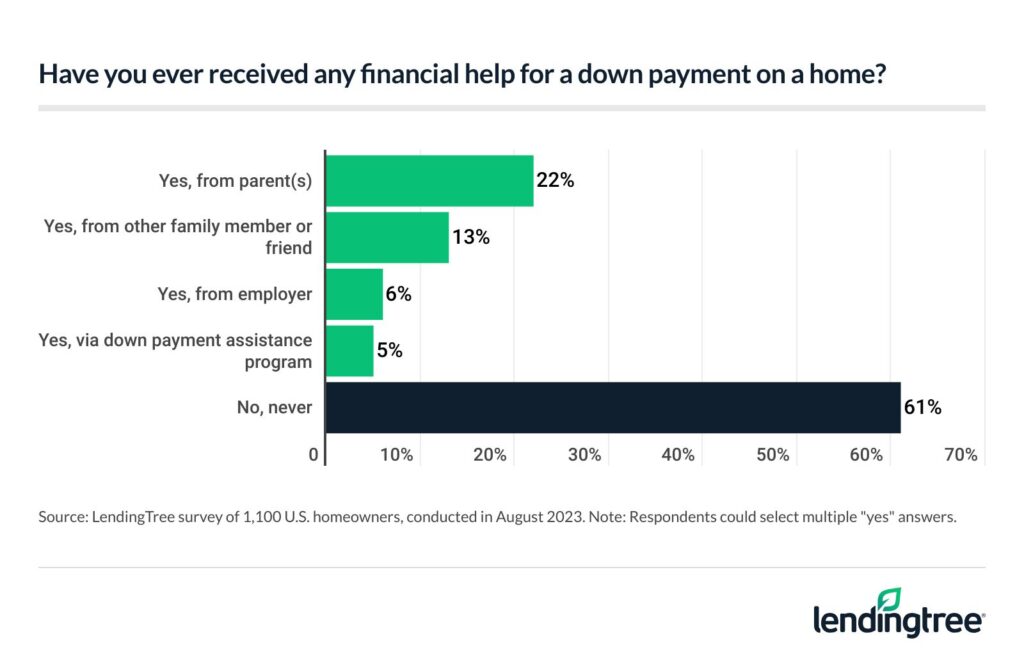

It’s not uncommon for younger and middle-aged buyers to ask their parents for help; the survey found that 22% of homeowners received downpayment assistance not through various assistance programs, but directly from their parents in the form of cash gifts.

Younger homeowners are the most likely to rely on others for help, at 78% among Gen Zers (ages 18 to 26). They’re also the group most likely to get help from their parents (49%). Following that (among homeowners):

- 54% of millennials (ages 27 to 42) have received help, with 27% getting it from their parents

- 33% of Gen Xers (ages 43 to 58) have received help, with 20% getting it from their parents

- 17% of baby boomers (ages 59 to 77) have received help, with 11% getting it from their parents

Meanwhile, homeowners with children younger than 18 (52%) are significantly more likely to have received help than those with no children (38%) and those with children older than 18 (23%). While parents with young children are most likely to rely on their parents for support (28%), 19% received aid from other family members or friends.

According to LendingTree senior economist Jacob Channel, receiving financial support should be seen as common, given the current market.

“In today’s housing market where — even if you can get approved for a loan — buying can still be prohibitively expensive, the more help you have with things like a down payment, the easier buying can be,” he says. “Ultimately, even though that figure is high (probably higher than many people would expect), it speaks to how expensive and tough to navigate today’s housing market can be.”

Click here to see LendingTree’s research in its entirety.