DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Climate-related hazards have emerged as crucial factors that influence home values in recent years; however, the impact of these risks on property prices remains concealed within their inherent value, according to a new CoreLogic report.

With the rise in the frequency of natural disasters, it is essential for lenders and insurance companies to accurately assess and quantify the risks associated with flooding in order to determine the costs involved. In the study, CoreLogic’s data science team will quantify the impact of Federal Emergency Management Agency (FEMA) flood zones on home prices by using regression analysis, while controlling for non-climate risk factors.

The Magnitude of Flood Risks in South Florida

Nearly 40% of total U.S. residents live in coastal regions, with Florida ranking among the top five states in terms of coastal population. Miami-Dade County stands out, being the seventh-most populated county in the U.S. A CoreLogic study indicates that approximately 41 million U.S. residents face the risk of flooding along rivers and streams, while 8.6 million individuals live in coastal areas with at least a 1% chance of flooding in any given year. If the current sea level rises by two feet, more than $1 trillion of property and structures are at risk, and roughly 50% of that vulnerable property value is in Florida.

Defining Flood Zones and the Effect on Home Sales in South Florida

For this analysis, CoreLogic experts examined residential sales data from the first quarter of 2011 to the second quarter of 2022 in Miami-Dade County. The sales data is sourced from CoreLogic, while flood-zone information was obtained from FEMA. By employing a spatial join in QGIS with FEMA’s flood-one shape files, CoreLogic assigned each property to a respective flood zone. This analysis uses a standard data-cleansing process, excluding flip sales and outlying transactions of explanatory variables.

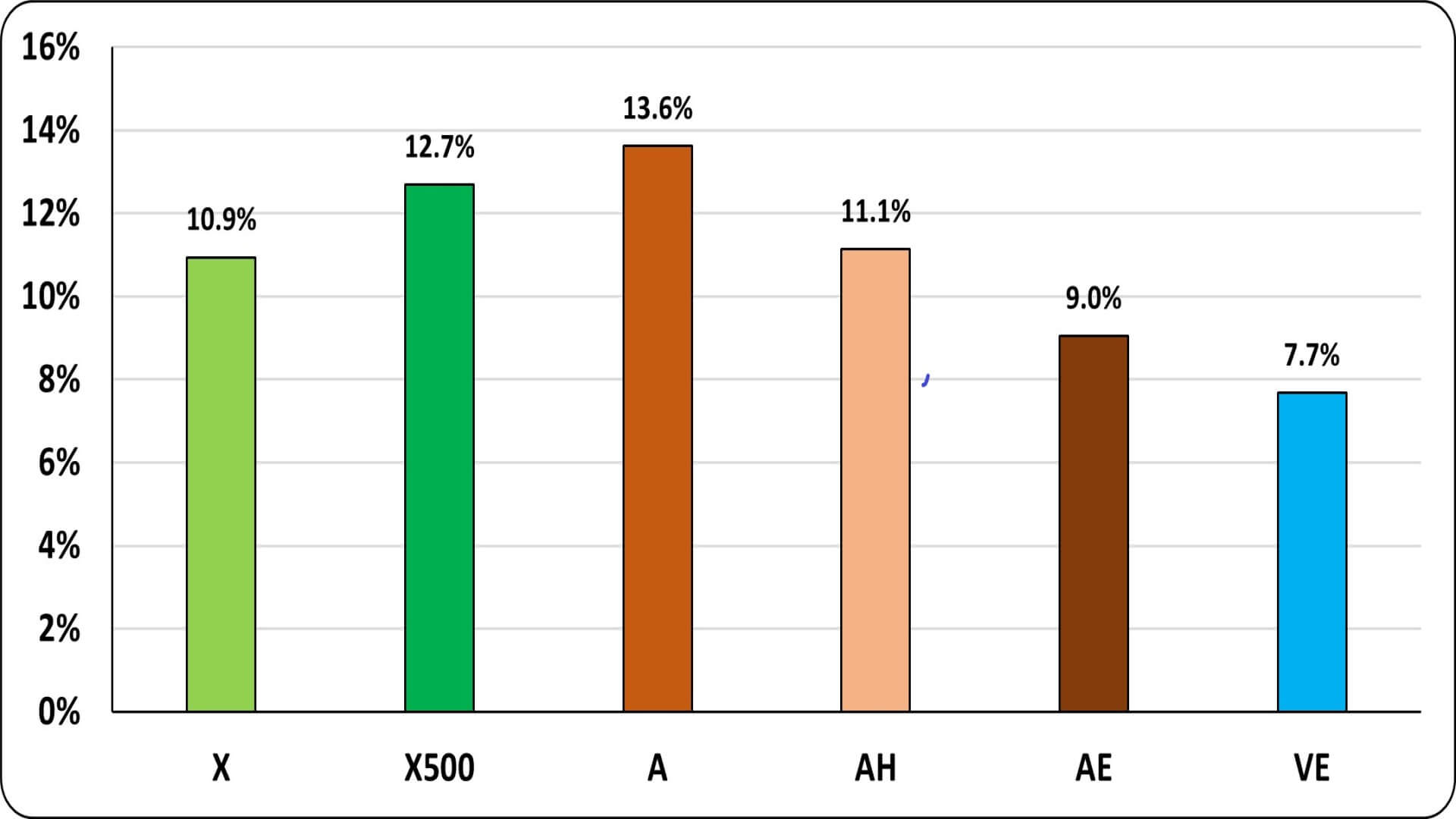

Flood zones in Miami-Dade County are defined as such:

- Zone X: An area that is determined to be outside the 100- and 500-year floodplains

- Zone X500 (Moderate flood risk): There is less than a 0.2% chance of annual flooding, or a 1 in 500 chance, which makes it one of the safest flood zones.

- Zone A (High flood risk): Because detailed analyses are not performed for such areas, no depths or base flood elevations are shown within these zones. In these areas, there is at least a 25% chance of flooding during a 30-year mortgage.

- Zone AE (Moderate-to-high flood risk): This is the flood zone area that corresponds with flood depths greater than three feet.

- Zone AH (Moderate-to-high flood risk): Areas with a 1% annual chance of shallow flooding, usually ponding, with an average depth ranging from one to three feet. These areas have a 26% chance of flooding over the life of a 30‐year mortgage.

- Zone VE (High flood risk): This is the flood zone area that corresponds to coastal areas that have additional hazards associated with storm waves. In these areas, there is at least a 25% chance of flooding during the span of a 30-year mortgage.

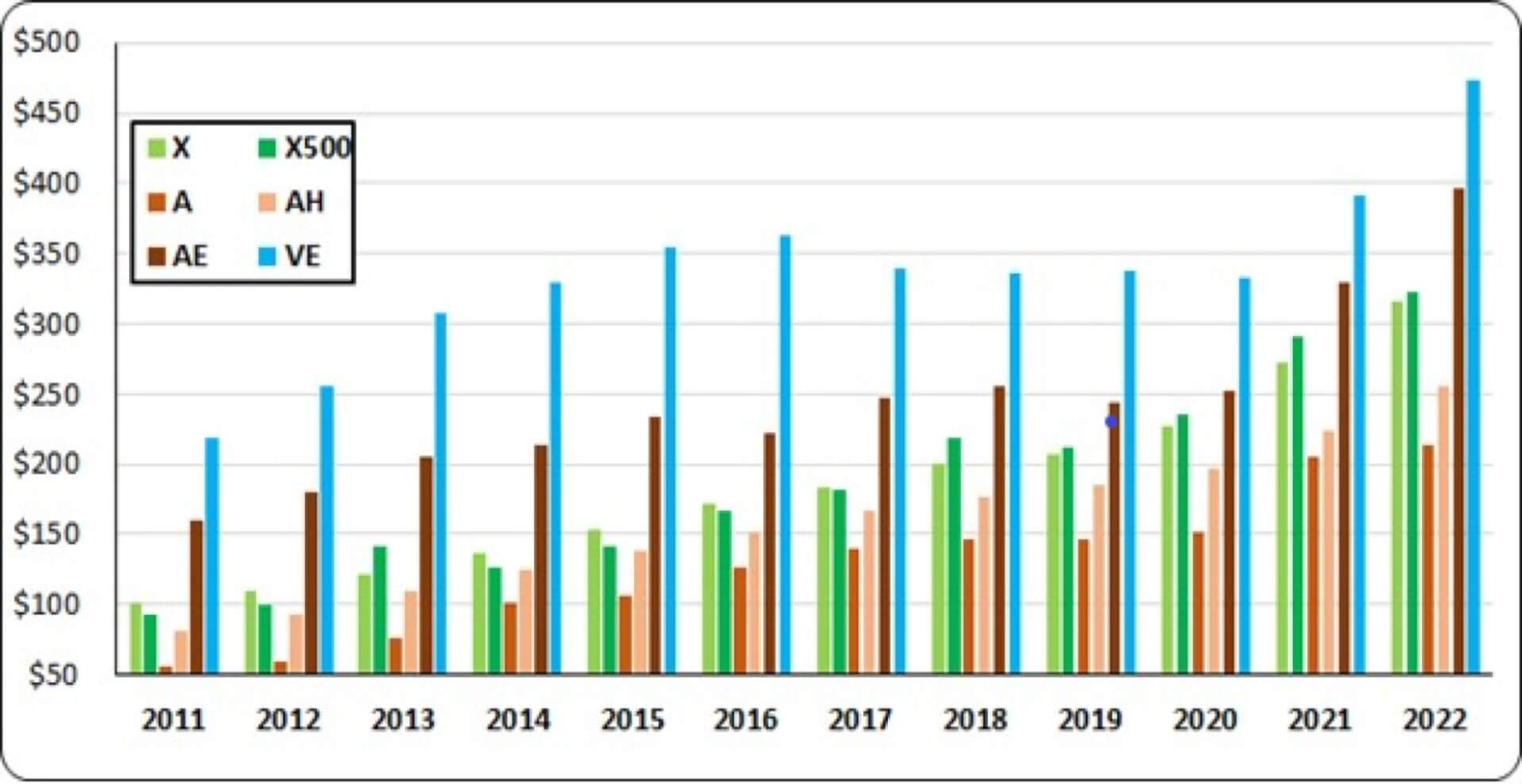

Coastal zones (VE) consistently command higher prices compared with other zones, with values that reached as high as $475 per square foot in 2022. Zone A properties, on the other hand, have the lowest prices, although their count is relatively small, with fewer than 50 properties in a given year.

There is minimal price differences between properties in the X and X500 zones. Within the inland flood zones (AE and AH), there is a significant disparity in the median price per square foot. At first glance, it appears that high flood risk translates to elevated home prices, which is counterintuitive.

By accounting for non-climate factors and isolating the true impact of climate risks, these risks indeed affect property prices, which are evident in the form of discounts. Given the projected increase in climate hazards, with an average of seven or eight events per year and an expected escalation in severity, it becomes crucial for lenders and insurers to adapt differential costs based on these risks.

To read the full report, including more data, charts, and methodology, click here.