DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

By current CoreLogic estimates, the recent landfall of Hurricane Ian caused anywhere between $41 to $70 billion in damage, marking the sixth consecutive year a slow-moving tropical system destroyed part of the country.

By current CoreLogic estimates, the recent landfall of Hurricane Ian caused anywhere between $41 to $70 billion in damage, marking the sixth consecutive year a slow-moving tropical system destroyed part of the country.

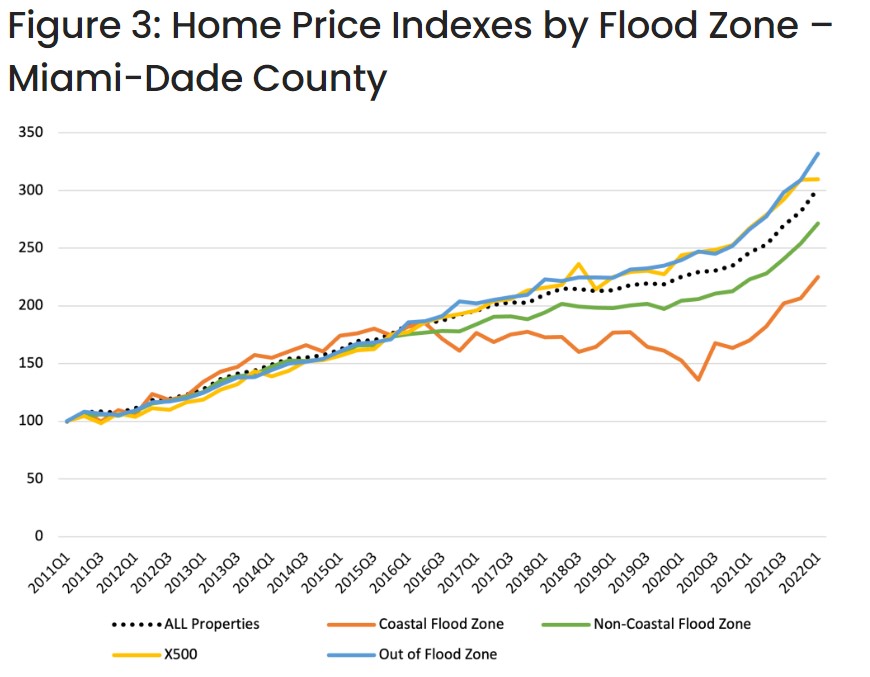

Climate change will only exacerbate severe weather events in the years to come, so CoreLogic asked the question, “What effect does flood risk have on a home’s value?” and studied property values in Miami to answer this question. Miami was chosen due to its vulnerability to hurricanes.

Buyers typically push for a discount on homes in Federal Emergency Management Agency (FEMA) flood zones to offset the cost of carrying government flood insurance, even when those homes have desirable features, such as being a waterfront property.

But there are certain risks some borrowers take when insuring their home—purchasing flood insurance is not mandated to receive a mortgage for a property outside of a 100-year flood zone, as designated by FEMA, even though its flood risk is not necessarily zero.

On the other hand, the study found that if borrowers are presented with a comprehensive flood risk model before buying, in return this could cause home values in flood-prone areas to drop as buyers move on to another property with less risk.

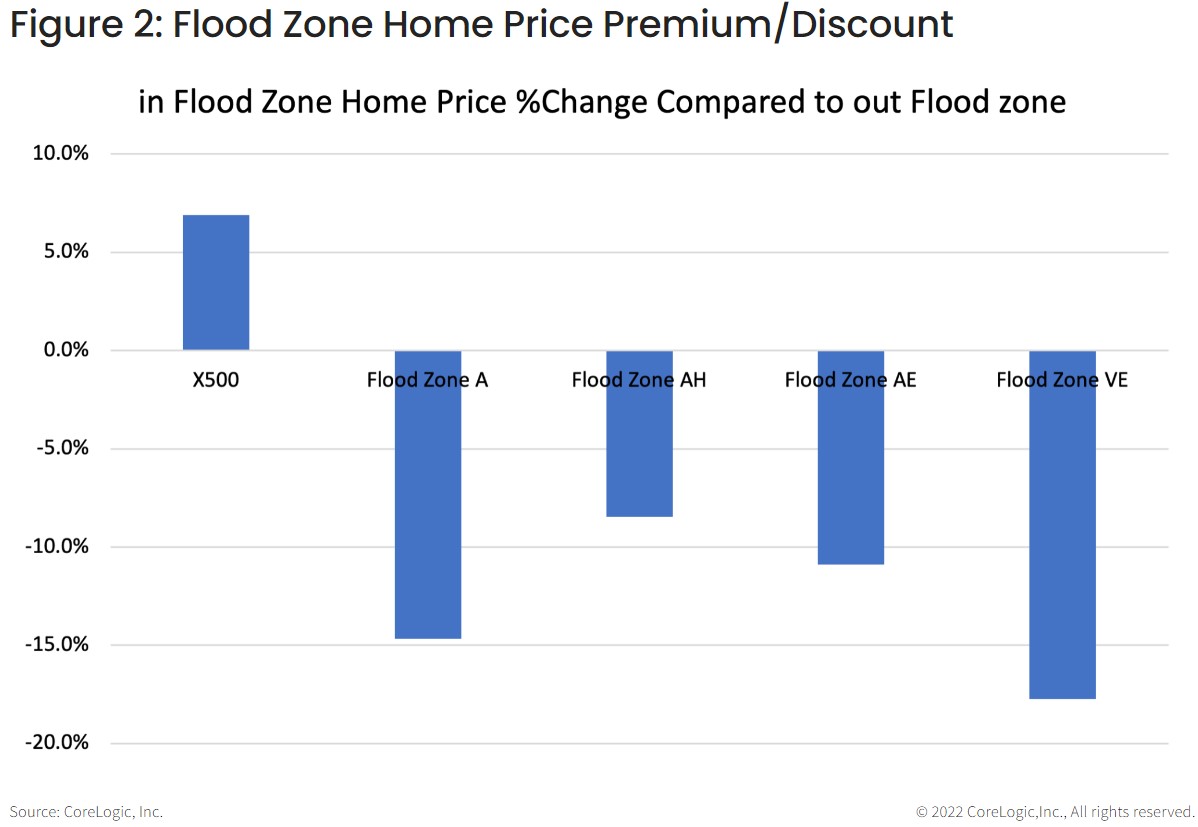

A Special Flood Hazard Area (SFHA) is defined as an area that will be inundated by a 1% annual chance of flood, which is also referred to as the base flood or 100-year flood. Zone X500 is a 500-year floodplain with a 0.2% of annual chance of flooding. Zone A, AE and AH are 100-year floodplains with a 1% of annual chance of flooding. Zone VE is for coastal areas with a 1% of annual chance of flooding and an additional hazard associated with storm waves. Zone X denotes areas of minimal flood hazard, which are areas outside the SFHA and higher than the elevation of the 0.2% annual chance of flooding.

“The above analysis clearly indicates a property in flood zones sells for less and appreciates slower over time than a similar property outside flood zones, given everything else is equal, in Miami,” said CoreLogic. “Is there any way to mitigate the risk and improve the property value? Building homes at a higher elevation will help. Regression results suggested that every foot of elevation can increase home value by 1.6% in a non-coastal flood zone. If not in a flood zone, every mile away from the 100-year floodplain can add 2.2% value to property. Being close to a fire station is another advantage since the fire service provides a vital role in responding to flood events.”

Click here to view more data and methodology on the research behind home location in a flood zone to property values in Miami.