DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

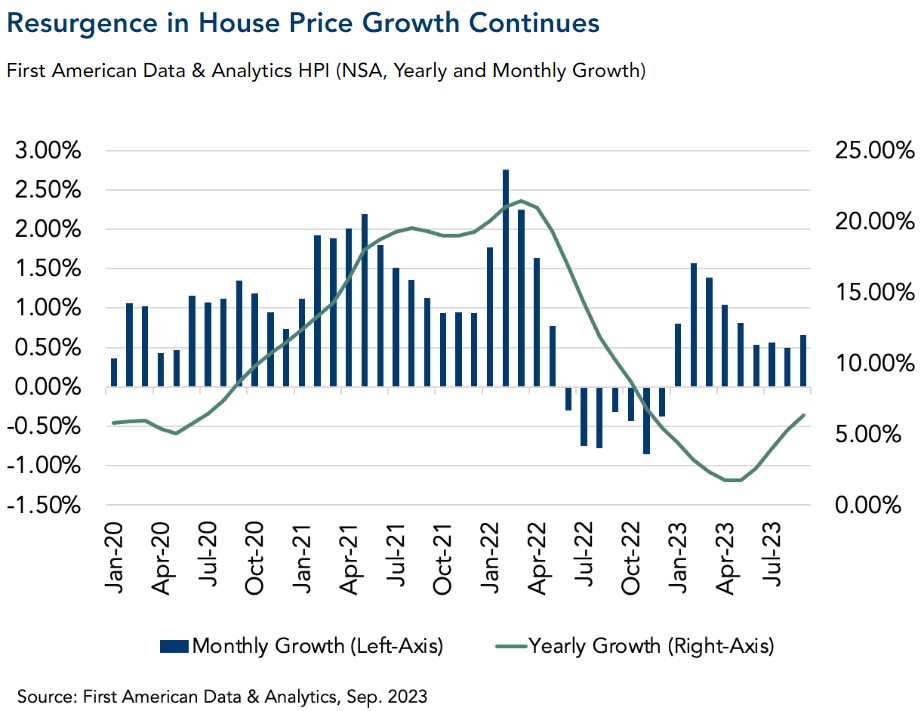

According to the latest edition of the Home Price Index (HPI) published by First American Data & Analytics, housing prices reached a new peak in September 2023 increasing 6.3% year-over-year and 0.7% from August 2023.

The report tracks home price changes across national, state, and metropolitan areas (as defined by the U.S. Census Bureau), and includes metropolitan price tiers that segment sales transactions into starter, mid, and luxury tiers.

The 0.7% month-over-month home price increase from August marks the sixth consecutive month that home prices have found a new peak.

“Rising mortgage rates continue to depress housing supply and suppress affordability, chilling the housing market. Preliminary September house price data suggests that the lack of supply is constraining the market more than reduced demand due to record-low affordability,” said Mark Fleming, Chief Economist at First American. “Nationally, house prices continue to set new records as potential sellers sit on the sidelines, limiting supply, while buyers chase what few homes are available for sale.”

The five most populous states experienced the following year-over-year growth in the HPI includes: Pennsylvania (+7.8%), New York (+4.4%), Florida (+3.5%), Texas (+3.5%), and California (+3.2%).

There were two states with a year-over-year decrease in the HPI: South Dakota (-11.2%) and Nevada (-0.7%).

Among the top-30 metropolitan areas, the five markets with the greatest year-over-year increase in the HPI are: Miami (+8.8%); St. Louis (+8.2%); Anaheim, California (+7.4%); San Diego (+7.1%); and Baltimore (+7.0%). Only two of the top-30 markets reported price declines: Austin, Texas (-3.8%) and Las Vegas (-0.9%).

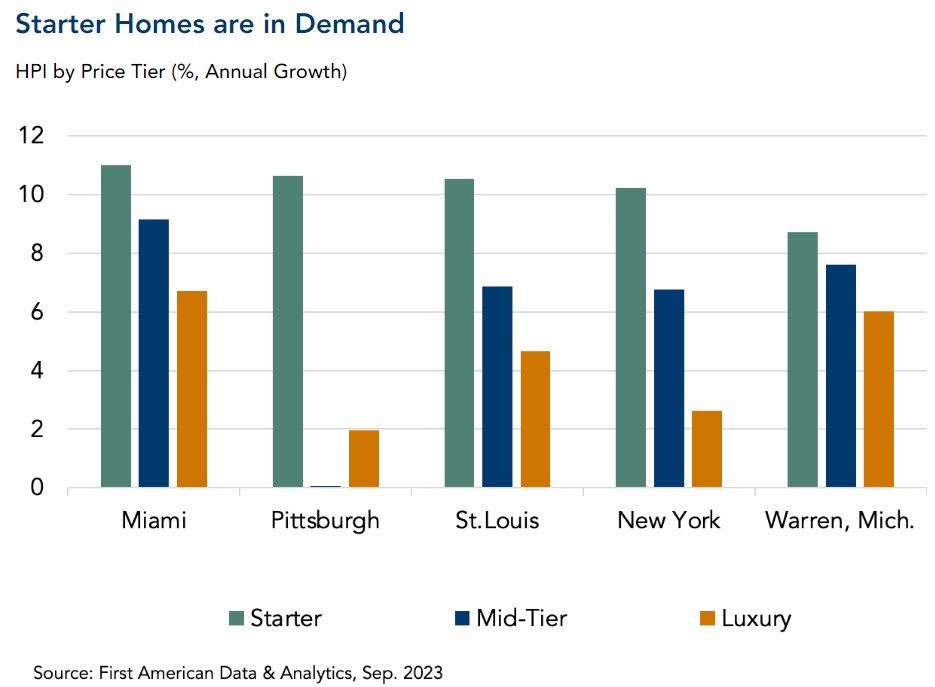

"The fact that the starter home price tier continues to outperform the middle and luxury price tiers in many markets suggests that first-time home buyer demand remains resilient despite significantly lower affordability," said Fleming. “As of 2022, more than half of all millennial households were homeowners, but many more are aging into their 30s, the prime home-buying age, and seeking to buy instead of rent. While less affordable than a year ago, the pace of starter tier price growth in markets like Miami, Pittsburgh and St. Louis suggests homeownership demand among millennials is far from dead."

Click here to see the report in its entirety.