DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

According to a new study from Point, despite record gains in home equity, many Americans cannot leverage the wealth they’ve earned from owning their home.

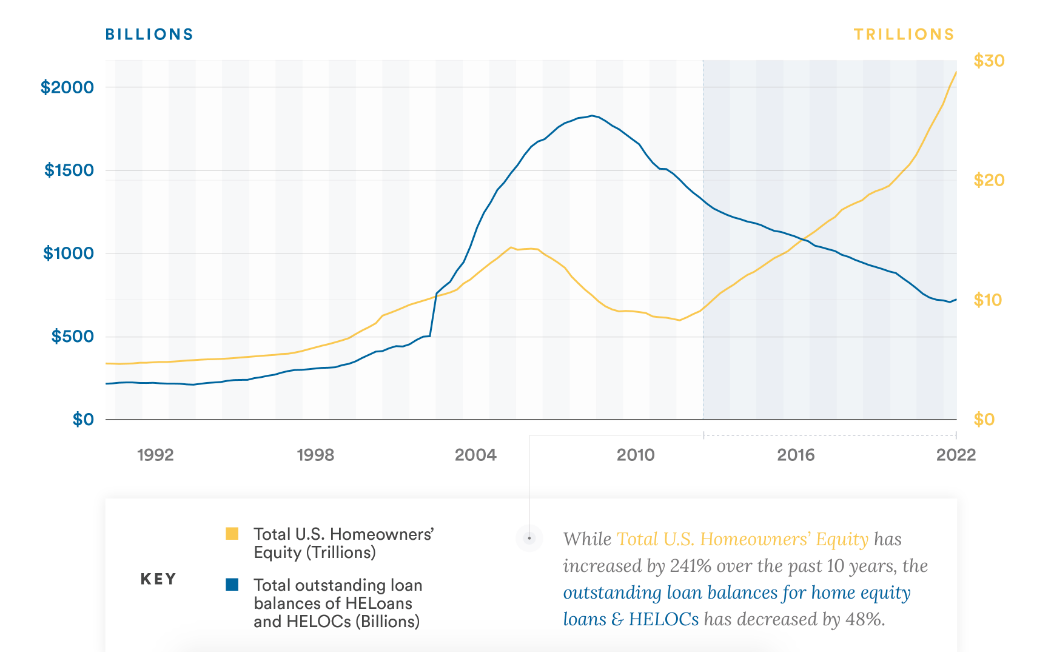

U.S. homeowners have more than $29.3 trillion in home equity–a 64% increase compared to the same time five years ago, yet many aren’t able to see these gains until they sell their homes. Homeowners have typically turned to traditional forms of financing, such as a cash-out refinance or a home equity line of credit (HELOC), to access their home equity for things like home renovations, starting businesses, or paying off higher-interest debt.

However, the current economic climate has made these options less accessible and attractive as rates have increased, and lending standards have tightened. As a result, while homeowners’ equity has increased by 241% over the past 10 years, the outstanding loan balances for home equity loans and HELOCs have decreased by 48% over the same period.

“Americans are feeling financial stress in various ways right now: credit card debt is at all-time highs, savings rates have dipped, and inflation has dramatically increased the cost of living,” said Eddie Lim, Co-Founder and CEO of Point. “However, homeowners are sitting on significant wealth they could use to improve their situations but don’t have a great option to access the wealth. It’s like we’ve all lost the PIN to our debit card–we have the money but don’t know how to access it.”

Cash-out refinances are significantly more expensive for homeowners now that mortgage rates are at their highest levels in 21 years, holding homeowners back. Take, for example, a homeowner who purchased the median-priced home for $310,600 in August 2020(2) with a 20% down payment. Given prevailing 2.91% 30-year fixed mortgage rates, the monthly payment was $1,035.

Three years later, the home value has increased 40% to $435,000, and the homeowner now has $204,661 of equity. They need to access $50,000 of this home equity for a home renovation, and their only option is a cash-out refinance. Given current mortgage rates of 7.19%, their monthly payment would more than double to $2,541.

HELOCs and home equity loans are another common way for all homeowners to tap their equity, particularly in a high-rate environment. However, nearly half of homeowners fail to qualify. The denial rate for HELOCs is 46%, compared to 12% for a conventional mortgage.

Credit scores can factor in HELOC denials: lenders generally require a credit score of at least 680 (although many prefer a score above 720), while 25% of Americans have a credit score under 650.

“It’s unfortunate so many homeowners are left behind when it comes to accessing their home equity,” added Lim. “Homeowners have earned their equity through diligence, hard work, and planning. They should have a path to leverage their equity even if they don't have perfect credit and a high income.”

To read the full report, including more data, charts, and methodology, click here.