DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

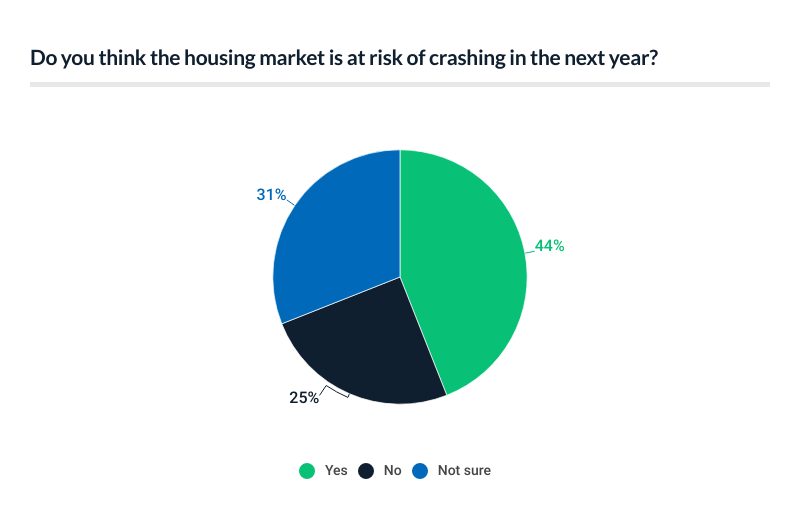

According to a new LendingTree survey of over 2,000 U.S. consumers, an estimated 44% of Americans think the housing market is at risk of crashing in the next year. On the other hand, with some non-homeowners believing a crash is the only way they could afford a home, it may not seem surprising that a grand 35% of Americans want the market to crash.

Key Findings:

- Most Americans aren’t optimistic about the housing market, with some hoping for a downturn. 44% of Americans think the housing market is at risk of crashing in the next year, with another 31% unsure. What’s more alarming is that 36% of homeowners and 35% of Americans overall want the market to crash. And while 51% of homeowners don’t want the market to burst, 15% of them say they want a crash to lower their property taxes and 15% believe it would lead to future stability.

- Nearly a third of non-homeowners think a crash is their only way to own a home. 32% of non-homeowners believe this, but that rises to 39% among Gen Zers and 38% among millennials who don’t own. Mortgage interest rates aren’t helping: Across all Americans, 53% are worried they’ll remain high. Separately, 79% expect rates to rise for at least another year. Looking ahead, 27% believe mortgage rates will be 8.00% or higher one year from now.

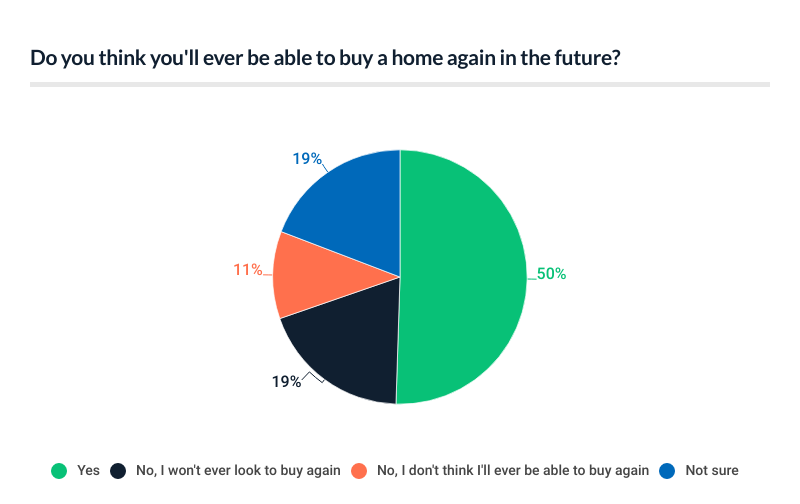

- Those who have a locked-in low rate may be stuck in their homes. Half (50%) of homeowners say their current rate is keeping them in their houses. In addition, three-fourths (75%) of Americans are unsure if they’ll ever see rates as low as in 2020 and 2021, and 11% of homeowners don’t think they’ll ever be able to buy a home again.

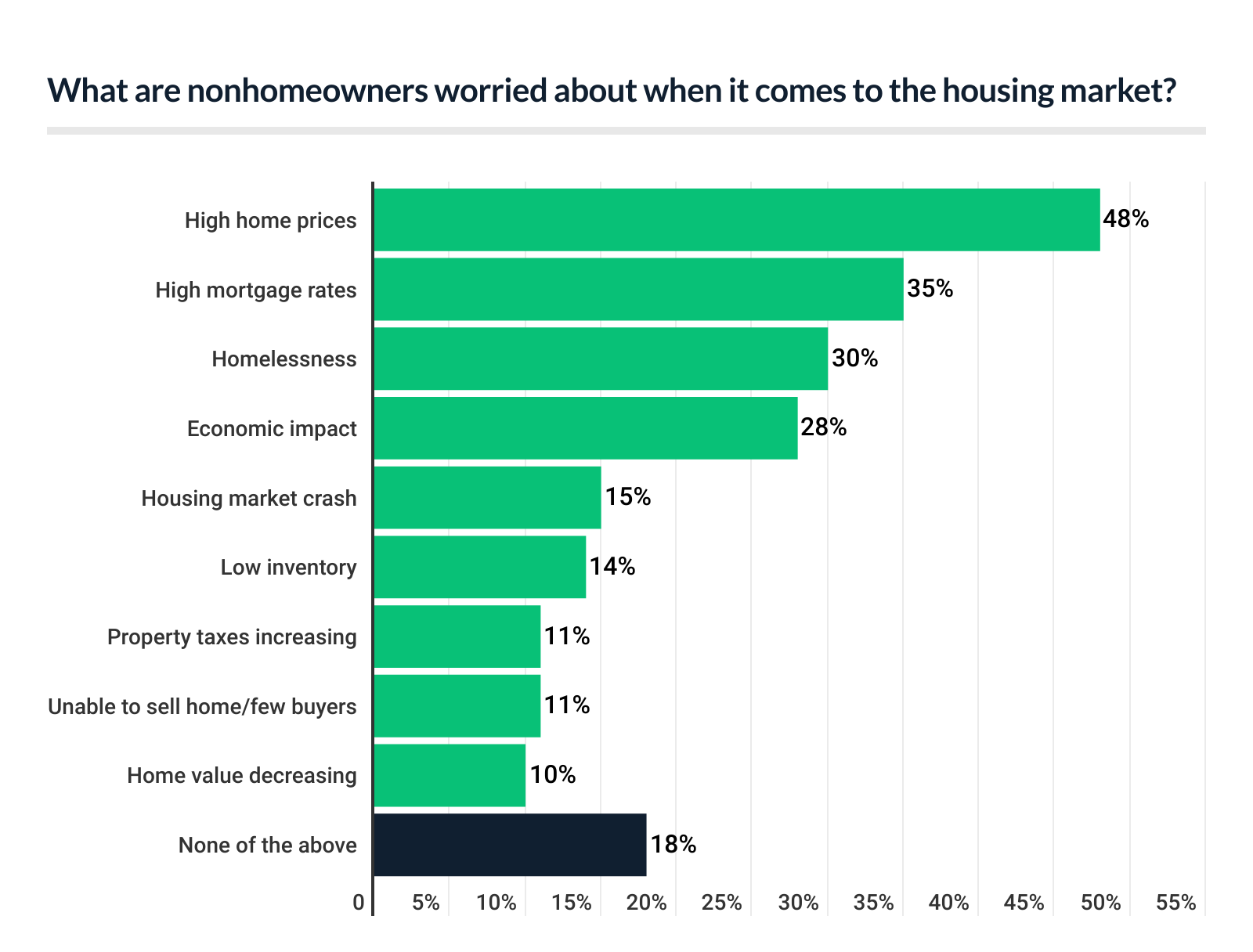

- Whether you rent or own, home prices and values are top of mind—for opposite reasons. When asked about their biggest housing market worries, non-homeowners cite high home prices (48%), while homeowners cite decreasing home values (38%). All in all, though, 62% of Americans think home prices will increase in the next year, with two-thirds (66%) of them believing they’ll rise by 5% or more.

Americans believe a housing crash is coming, and some are looking forward to it.

It’s been a difficult year for consumers looking to buy a home, with 30-year mortgage rates reaching nearly 8.00% in October 2023 — the highest since November 2000. Those figures are certainly weighing heavily on most Americans: In fact, 44% think the housing market is at risk of crashing in the next year, while another 31% are unsure.

Millennials (ages 27 to 42) are the most likely age group to believe a market crash is coming, at 52%. That’s followed by:

- Gen Zers (ages 18 to 26) (48%)

- Gen Xers (ages 43 to 58) (42%)

- Baby boomers (ages 59 to 77) (30%)

In addition, those with children younger than 18 (55%) are more likely to expect a market crash than those without children (39%) and those with children older than 18 (35%). Meanwhile, homeowners (46%) are slightly more likely to think a market crash is coming than nonhomeowners (41%).

But not everyone thinks a market crash would be bad, though: 36% of homeowners want the market to crash. Among this group, 15% of them say they want a crash to lower their property taxes and 15% believe it would lead to future stability.

More broadly speaking, 35% of Americans want the market to crash. That’s especially true among Gen Zers (53%), millennials (46%) and those with children younger than 18 (46%). On the other hand, baby boomers (18%) and those with children older than 18 (22%) are the least likely to share this feeling.

LendingTree Senior Economist Jacob Channel isn’t surprised that so many people want the market to crash, but he’s skeptical about whether they know what it would mean.

“Right now, home prices are high, as are mortgage rates,” said Channel. “With that in mind, I can understand why some might wish for a housing crash that brings lower prices. Unfortunately, if the national housing market were to crash, odds are that it would bring down the rest of the economy with it.”

However, Channel believes there’s hope for potential homebuyers.

“It’s not impossible for home prices to fall and make a given housing market more affordable,” he said. “It’s also not necessarily impossible for the housing market to outright crash next year while the rest of the economy remains relatively OK (though it’s very unlikely). But if you’re hoping that the housing market will crash and make it easier for you to buy a house, you’ll probably be disappointed. Not only does data indicate the odds of a housing crash in the next few years are slim, the past shows that when the market crashes, it tends to hurt more people than it helps.”

Some non-homeowners believe a housing market crash is the only way they could buy a home.

Despite the potential consequences of a market crash, 32% of non-homeowners believe a downturn is the only way they could afford a home. That’s particularly true among young Americans—39% of Gen Zers and 38% of millennials who don’t own. Across all demographics, those earning $50,000 to $79,999 (41%) and those with children younger than 18 (39%) are also among the most likely to share this sentiment.

Mortgage interest rates likely play a large role, though nonhomeowners aren’t the only ones worried. The average rate for a 30-year fixed mortgage was 7.50% as of the week of Nov. 9, and 53% of Americans are worried rates will remain high.

That’s particularly true among those with children younger than 18 (61%), those earning $75,000 to $99,999 (60%) and millennials (59%). In addition, women (56%) are more worried about high interest rates than men (49%).

Separately, 79% expect rates to rise for at least another year, with 53% of this group believing rates will rise for over a year or longer. Regardless of how long they expect rates to rise, though, 27% of Americans believe mortgage rates will be 8.00% or higher a year from now. Beyond that:

- Approximately 19% believe mortgage rates will be between 5.00% and 5.99%

- Some 15% believe mortgage rates will be between 6.00% and 6.99%

- Roughly 13% believe mortgage rates will be between 7.00% and 7.99%

Gen Zers are the most optimistic age group, with 21% thinking rates will be between 5.00% and 5.99%. Meanwhile, 21% of baby boomers think rates will be between 7.00% and 7.99%.

While it’s difficult to predict what mortgage rates will look like in the future, Channel reported there is reason to believe rates will go down next year.

“Across the board, interest rates have risen dramatically since the start of 2022, and mortgage rates are no exception,” he said. “Fortunately, just because rates have risen over the last two years doesn’t mean they’ll continue to climb in 2024. On the contrary, there are encouraging signs, like cooling inflation, that could help bring down rates next year. If inflation continues to cool and the Fed starts cutting rates in 2024 (as they appear poised to do), rates should fall. They won’t plummet, but they might end up closer to 6.00% or 7.00% than 8.00% or higher.”

Some homeowners with low mortgage rates are feeling stuck.

It’s not just non-homeowners struggling with rising rates—homeowners believe they have implications for them, too. Among this group, 50% say their current rate is keeping them in their houses and they don’t want to get financing on a new house. That’s especially true for homeowners with kids younger than 18 and millennial homeowners, at 64% and 61%, respectively.

Overall, Americans believe 2020 and 2021 was a once-in-a-lifetime opportunity for homebuying, when mortgage rates were between 2.65% and 3.72%. Three-fourths (75%) of Americans say they aren’t sure if they’ll ever see rates as low as in 2020 and 2021—a figure that rises to 82% among those earning $50,000 to $74,999, 81% among women and nonhomeowners, and 78% among baby boomers and those without children.

With these beliefs in mind, 11% of homeowners don’t think they’ll ever be able to buy a home again and 19% are unsure.

“There’s a chance that they could fall back to their 2020 and 2021 levels again at some point, just as there’s a chance they’ll spike back up to their early 1980s levels,” said Channel. “From where things stand, I’d say that either scenario is more unlikely than not.”

While Channel believes rates will come down over the next few years, he says he’d be genuinely shocked if they fall to their height-of-the-pandemic record lows: “Unless something catastrophic—like another major pandemic or a meteor crashing into Manhattan—I think people are right to assume rates aren’t going to fall to sub-3.00% levels anytime soon, if ever.”

To read the full report, including more data, charts, and methodology, click here.