DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

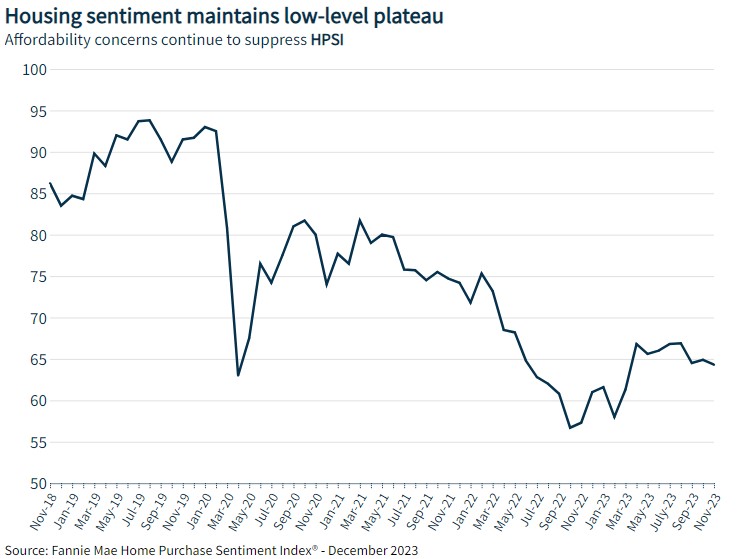

According to the new Fannie Mae Home Purchase Sentiment Index (HPSI), the number of people who think now is a good time to buy a home dropped a minor 0.6 points in November, a number that remains with the bounds of a recent plateau that first emerged during the first half of 2023.

According to the new Fannie Mae Home Purchase Sentiment Index (HPSI), the number of people who think now is a good time to buy a home dropped a minor 0.6 points in November, a number that remains with the bounds of a recent plateau that first emerged during the first half of 2023.

Pessimism has overtaken the homebuying market as only 14% of consumers believe it’s a good time to buy a home, which represents a new low for the survey.

Pluralities of respondents also continue to expect both home prices and mortgage rates to increase over the next 12 months.

Overall, the full index is up 7.0 points compared to this time last year.

“Over the past year, the HPSI has plateaued at a low level, evidence of persistent consumer pessimism regarding the state of the housing market,” said Doug Duncan, Fannie Mae SVP and Chief Economist. “Looking back, consumer belief that it’s a ‘bad time to buy a home’ hit a survey high several times this year—including this month—and each time the pessimism could be attributed to high home prices and high mortgage rates.”

“At the end of 2022, as mortgage rates approached 7%, a rate level not seen in over a decade, a plurality of consumers said they expected home prices to decrease; however, that optimism faded over the course of 2023,” Duncan continued. “A significant majority of respondents have also continued to expect mortgage rates to increase or stay the same, though these expectations have tempered over the year. At the same time, consumers have expressed a reduced sense of financial security, with fewer respondents reporting household income growth over the year and a higher percentage saying their incomes remained the same.”

“The combination of persistent affordability challenges and less rosy household finances remain the primary drivers of the low-level plateauing of housing sentiment. Even if mortgage rates decline over the next year, which we currently expect, it’s unlikely to meaningfully affect affordability,” Duncan concluded. “The lack of housing inventory is likely to remain a challenge for some time, and home purchase sentiment may continue to be suppressed as a result. As our forecast indicates, we believe it will be a couple years before homes sales return to more normal, pre-pandemic levels.”

By the numbers, the HPSI decreased 0.6 points from October to an index level of 64.3%; this number is up 7 points compared to the same time last year.

High level data, as highlighted by Fannie Mae, includes:

- Good/Bad Time to Buy: The percentage of respondents who say it is a good time to buy a home decreased from 15% to 14%, while the percentage who say it is a bad time to buy remained unchanged at 85%. As a result, the net share of those who say it is a good time to buy decreased 1 percentage point month-over-month.

- Good/Bad Time to Sell: The percentage of respondents who say it is a good time to sell a home decreased from 63% to 60%, while the percentage who say it’s a bad time to sell increased from 37% to 40%. As a result, the net share of those who say it is a good time to sell decreased 5 percentage points month-over-month.

- Home Price Expectations: The percentage of respondents who say home prices will go up in the next 12 months increased from 40% to 41%, while the percentage who say home prices will go down increased from 23% to 24%. The share who think home prices will stay the same decreased from 36% to 35%. As a result, the net share of those who say home prices will go up in the next 12 months remained unchanged month-over-month.

- Mortgage Rate Expectations: The percentage of respondents who say mortgage rates will go down in the next 12 months increased from 16% to 22%, while the percentage who expect mortgage rates to go up decreased from 47% to 44%. The share who think mortgage rates will stay the same decreased from 36% to 34%. As a result, the net share of those who say mortgage rates will go down over the next 12 months increased 8 percentage points month-over-month.

- Job Loss Concern: The percentage of respondents who say they are not concerned about losing their job in the next 12 months decreased from 78% to 76%, while the percentage who say they are concerned increased from 21% to 23%. As a result, the net share of those who say they are not concerned about losing their job decreased 4 percentage points month-over-month.

- Household Income: The percentage of respondents who say their household income is significantly higher than it was 12 months ago decreased from 20% to 19%, while the percentage who say their household income is significantly lower increased from 10% to 12%. The percentage who say their household income is about the same decreased from 69% to 68%. As a result, the net share of those who say their household income is significantly higher than it was 12 months ago decreased 3 percentage points month-over-month.

Read the full research report for additional information.