DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

As the New Year approaches, the market is cooling and improving in more ways than one. New listings and pending home sales both climbed to the highest level in roughly a year in November as homebuyers and sellers got tired of waiting on the sidelines and mortgage rates ticked down.

That’s according to a new report from Redfin, which showed home prices also jumped, posting the biggest year-over-year increase since late 2022.

New listings rose 1.3% month-over-month to the highest level since October 2022—on a seasonally adjusted basis—and increased 0.1% from a year earlier. While this is a small gain, it is the first in a year and a half. Active listings grew 3.9% month-over-month, representing the biggest increase since July 2022, although they fell 7.9% from a year earlier.

“Buyers and sellers are learning to live with uncertainty,” said Shay Stein, a Redfin Premier real estate agent in Las Vegas. “They’ve realized no one has a crystal ball that can predict exactly when mortgage rates will fall back to 5%, so they’re making moves now because they can only wait so long to be near their grandkids, live in an RV like they’ve always dreamt of, or finalize their divorce.”

While rates aren’t back to the softer 5% rate, they have fallen in recent weeks, which has motivated homebuyers, said Stein. In many cases, their monthly payment is $200 less than it would’ve been had they locked in a rate three weeks ago when they started looking, she explained.

The average 30-year-fixed mortgage rate declined every week in November after hitting a 23-year high of 7.79% at the end of October. It ended November at 7.22% and currently stands at 6.95%, though that’s still higher than the 6.3% rate of a year ago.

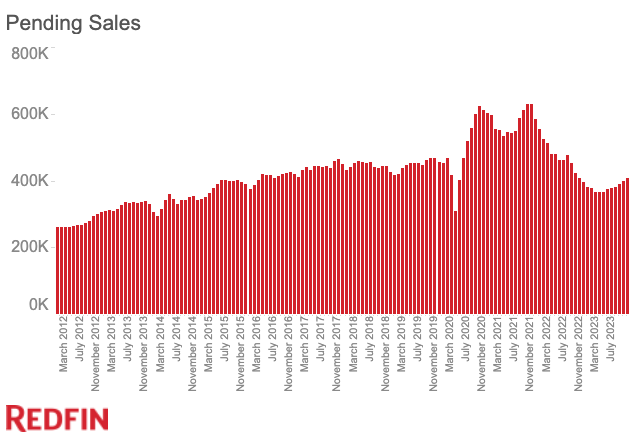

Pending home sales rose 2% month-over-month in November to the highest level in a year on a seasonally adjusted basis and fell 0.1% from a year earlier.

“Another reason sales are ticking up is that buyers and sellers are finally living in the same reality,” said Stein. “A year ago, sellers had trouble understanding why they weren’t getting $20,000 over the list price like their neighbor did during the pandemic homebuying boom. Now, they understand that to sell their home, they need to price it fairly and, in some cases, offer the buyer concessions like money toward closing costs or mortgage-rate buydowns.”

Home Prices Posted the Biggest Increase Since October 2022

The median U.S. home sale price was $408,732 in November. That’s up 3.7% from a year earlier—the biggest jump since October 2022—and down 1.1% from a month earlier.

Annual home price growth seems to be normalizing after prices surged as much as 26% at the height of the pandemic homebuying boom and then fell as much as 4% in early 2023 amid elevated mortgage rates. Price growth is now back to the 2%–7% range it was in prior to the pandemic.

Even though elevated mortgage rates have dampened demand in recent months, prices have continued to rise in part because buyers are competing for a limited number of homes. While listings have inched up in recent months, they remain low by historical standards.

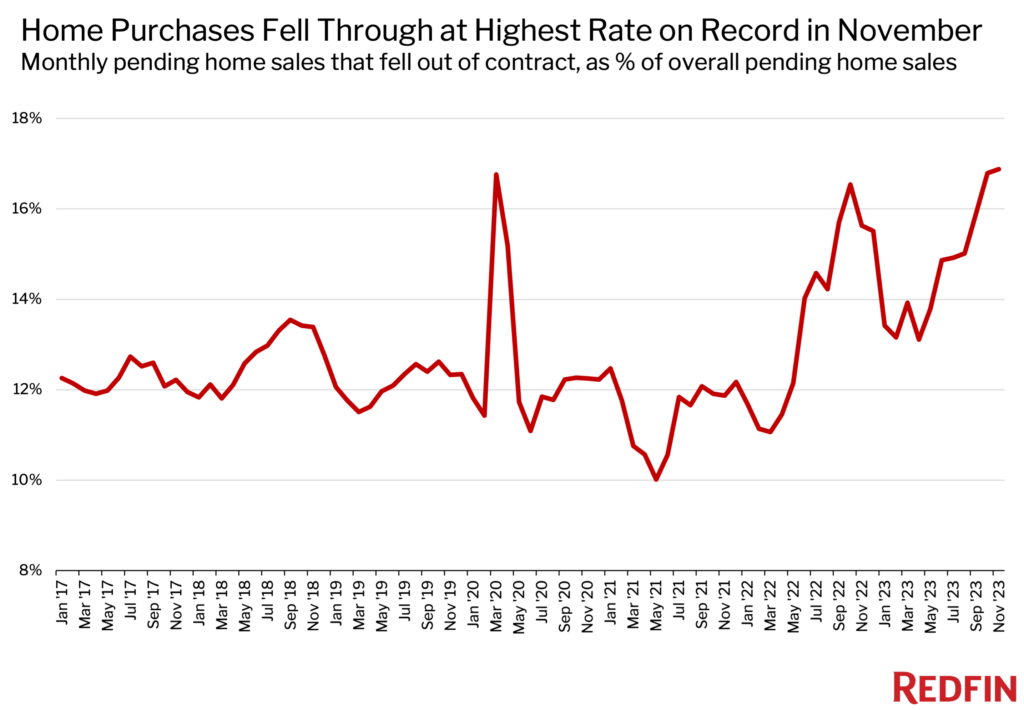

Purchases Fell Through at Record Rate as Some Buyers Got Cold Feet

While pending sales hit the highest level in a year in November, closed sales hovered near their recent low. They were little changed from a month earlier (0.2%) on a seasonally adjusted basis and fell 5.4% from a year earlier. That’s partly because a lot of deals fell through at the last minute.

Roughly 45,000 U.S. home-purchase agreements were canceled in November, equal to 16.9% of homes that went under contract that month—the highest percentage in Redfin records that date back to 2017. That’s up from 16.8% one month earlier and 15.6% one year earlier.

Key Findings for November 2023:

- The median sale price was $408,732, representing a month-over-month (MoM) change of -1.1% and a year-over-year (YoY) change of 3.7%.

- Pending sales (seasonally adjusted) were, 406,687, representing a MoM change of 2% and a YoY change of -0.1%.

- Homes sold (seasonally adjusted) were 411,958, representing a MoM change of 0.2% and a YoY change of -5.4%.

- New listings (seasonally adjusted) were 504,263, representing a MoM change of 1.3% and a YoY change of 0.1%.

- All homes for sale (active listings) sat at 1,504,094, representing a MoM change of 3.9% and a YoY change of -7.9%.

- Months of supply was 2.9, representing a MoM change of 0.2 days and a YoY change of -0.1 days.

- Median days on market was 36, representing a MoM change of 2 days and a YoY change of -1 days.

- The share of for-sale homes with a price drop was 18.7%, representing a MoM change of -1.3 percentage points and a YoY change of -0.7 percentage points.

- The share of homes sold above final list price was 28.7%, representing a MoM change of -3 percentage points and a YoY change of +2.3 percentage points.

- The average sale-to-final-list-price ratio was 99%, representing a MoM change of -0.3 percentage points and a YoY change of +0.5 percentage points.

- Pending sales that fell out of contract, as % of overall pending sales, was 16.9%, representing a MoM change of +0.1 percentage points and a YoY change of +1.3 percentage points.

- The average 30-year fixed mortgage rate sat at 7.44%, representing a MoM change of -0.18 percentage points and a YoY change of +0.63 percentage points.

Metro-Level Highlights for November 2023:

- Pending sales: In Anaheim, CA, pending sales rose 18.7% year over year, more than any other metro Redfin analyzed. Next came San Antonio (16%) and Richmond, VA (14.5%). The biggest declines were in Greensboro, NC (-30.2%), Birmingham, AL (-27.6%), and Knoxville, TN (-27.4%).

- Closed sales: Closed sales climbed from a year earlier in just six metros, with the biggest increases in North Port, FL (26.1%), Orlando, FL (6.3%), and Cape Coral, FL (5.3%). They fell most in Tacoma, WA (-35.1%), Nassau County, NY (-20%), and New York (-19.7%).

- Prices: Median sale prices rose most from a year earlier in Rochester, NY (17.9%), Anaheim (17.7%), and Fort Lauderdale, FL (13.5%). They fell most in Austin, TX (-8.8%), San Antonio (-6.2%), and New Orleans (-3.7%).

- Listings: New listings rose most from a year earlier in North Port (34.1%), Omaha, NE (29.3%), and Cape Coral (22.5%). They fell most in Honolulu (-18%), Atlanta (-15.3%), and Greensboro (-13.9%).

- Supply: Active listings increased fastest in Cape Coral (50.7%), North Port (39.2%), and New Orleans (24.2%). They decreased the fastest in Las Vegas (-34.7%), Stockton, CA (-28.1%), and New Brunswick, NJ (-24.6%).

- Competition: In Rochester, 70.4% of homes sold above their final list price, the highest share among the metros Redfin analyzed. Next came Newark, NJ (62.2%) and Buffalo, NY (59.7%). The shares were lowest in West Palm Beach, FL (8.9%), Cape Coral (10.1%), and New Orleans (11.5%).

- Speed: In Rochester, 66.2% of homes that went under contract did so within two weeks—the highest share among the metros Redfin analyzed. Next came Buffalo (52.8%) and Cincinnati (51.4%). The lowest shares were in Honolulu (5.7%), Knoxville, TN (9.3%), and Lake County, IL (10.1%).

While some homebuyers and sellers have come to terms with today’s economic uncertainty, that same uncertainty is causing many of them to get cold feet, Stein said. Even though mortgage rates have dropped, housing affordability remains strained, meaning a lot of buyers still get nervous when they see their monthly payment on paper.

Overall, economic woes are keeping many people out of the housing market altogether. Many Americans feel that the economy is in a bad place despite economic growth, rising wages, and low unemployment. One obvious culprit is the housing market, which is in its least affordable year on record.

To read the full report, including more data, charts, and methodology, click here.