DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

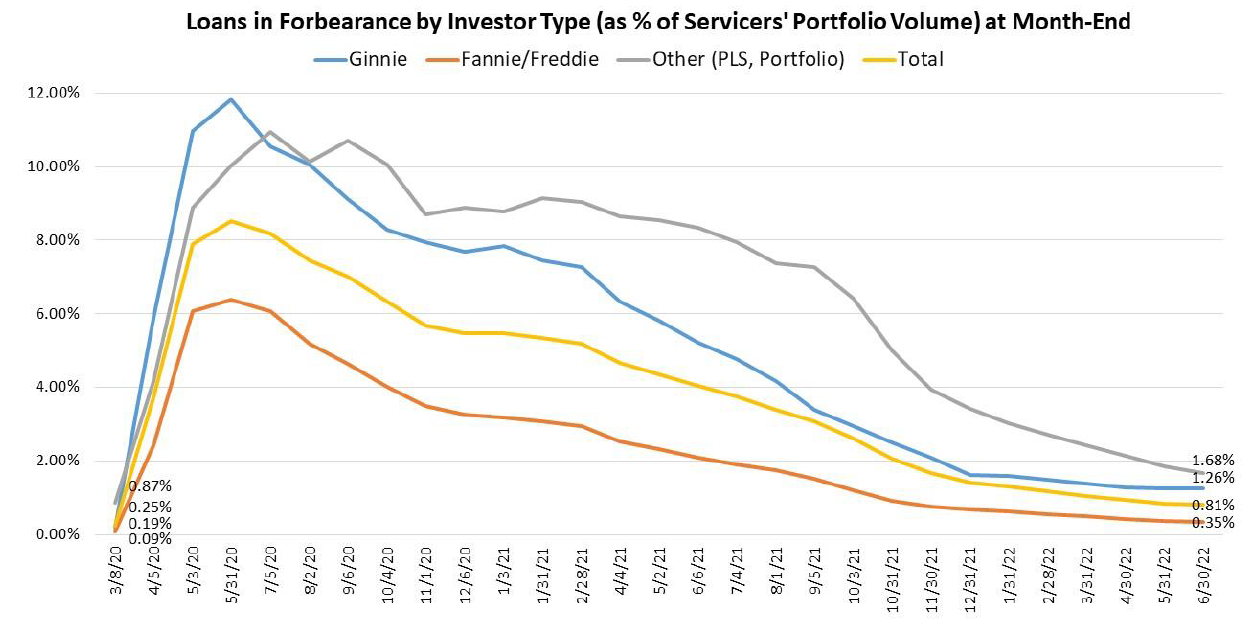

The latest Loan Monitoring Survey from the Mortgage Bankers Association (MBA) has found the total number of loans now in forbearance nationwide decreased by just four basis points, from 0.85% of servicers’ portfolio volume in the prior month to 0.81% as of June 30, 2022. Approximately 405,000 homeowners in the U.S. remain in forbearance plans.

The latest Loan Monitoring Survey from the Mortgage Bankers Association (MBA) has found the total number of loans now in forbearance nationwide decreased by just four basis points, from 0.85% of servicers’ portfolio volume in the prior month to 0.81% as of June 30, 2022. Approximately 405,000 homeowners in the U.S. remain in forbearance plans.

“The overall forbearance rate in June stayed relatively flat with just a 4-basis-point decline from May,” said Marina Walsh, CMB, MBA’s VP of Industry Analysis. “Borrowers continue to exit forbearance, but at a much slower pace than six or nine months ago. New forbearance requests are still trickling in, as permitted under the CARES Act, resulting in very little movement in the overall percentage of loans in forbearance.”

The Coronavirus Aid, Relief, and Economic Security (CARES) Act (2020) was passed by Congress on March 25, 2020, and signed into law on March 27, 2020, implementing a number of programs to address issues related to the onset of the COVID-19 pandemic. The Consolidated Appropriations Act continued many of these programs by adding new phases, new allocations, and new guidance to address issues related to the continuation of the COVID-19 pandemic.

By stage, 29.8% of total loans in forbearance were in the initial forbearance plan stage, while 57.6% were in a forbearance extension. The remaining 12.6% were forbearance re-entries, including re-entries with extensions.

By loan type, the share of Fannie Mae and Freddie Mac loans in forbearance decreased three basis points from 0.38% to 0.35% in June. Ginnie Mae loans in forbearance increased one basis point, from 1.25% to 1.26%, while the forbearance share for portfolio loans and private-label securities (PLS) declined 18 basis points, from 1.86% to 1.68%.

With inflationary concerns still top-of-mind for most Americans, last week’s unemployment report from the U.S. Department of Labor (DOL) painted a bit of a bleak picture. For the week ending July 9, the advance figure for seasonally adjusted initial claims stood at 244,000, an increase of 9,000 from the previous week's unrevised level of 235,000. The four-week moving average was 235,750, an increase of 3,250 from the previous week's unrevised average of 232,500. Meanwhile, the advance seasonally adjusted insured unemployment rate was 0.9% for the week ending July 2, a decrease of 0.1 percentage point from the previous week's unrevised rate.

Adding to a loss of jobs nationwide was last week’s rise in mortgages rates as Freddie Mac reported in its Primary Mortgage Market Survey (PMMS) report, that the 30-year fixed-rate mortgage (FRM) jumped back up to 5.51% after a huge drop-off the previous week.

Of the cumulative forbearance exits for the two-year period from June 1, 2020, through June 30, 2022, at the time of forbearance exit:

- 29.4% resulted in a loan deferral/partial claim

- 18.5% represented borrowers who continued to make their monthly payments during their forbearance period

- 17.2% represented borrowers who did not make all their monthly payments and exited forbearance without a loss mitigation plan in place yet.

- 15.8% resulted in a loan modification or trial loan modification

- 11.2% resulted in reinstatements, in which past-due amounts are paid back when exiting forbearance

- 6.7% resulted in loans paid off through either a refinance or by selling the home

- The remaining 1.2% resulted in repayment plans, short sales, deed-in-lieus or other reasons.

“There are some early indicators of borrower stress resulting from high inflation and rising interest rates, among other factors,” added Walsh. “For example, overall servicing portfolio performance dropped by 14 basis points to 95.71% current in June, and the performance of post-forbearance workouts declined by 140-basis points to 81.34%. It is worth monitoring post-forbearance workouts for all borrowers, and particularly for borrowers with government loans, who are typically the most vulnerable to economic slowdowns.”

Regionally, the five states reporting the highest share of loans current as a percent of servicing portfolio included:

- Idaho

- Washington

- Utah

- Colorado

- Oregon

The five states reporting the lowest share of loans current as a percent of servicing portfolio in June included:

- Mississippi

- Louisiana

- New York

- West Virginia

- Illinois