DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

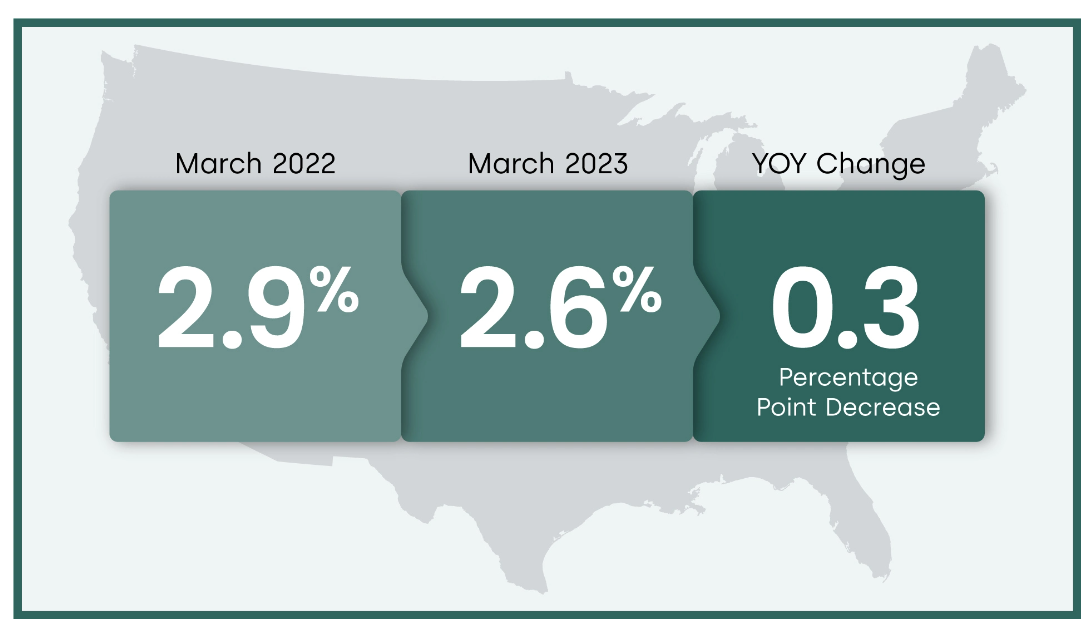

CoreLogic has released its monthly Loan Performance Insights Report for March 2023, which found that 2.6% of all mortgages nationwide were in some stage of delinquency (defined as 30 days or more past due, including those in foreclosure), representing a 0.3-percentage point decrease, compared to 2.9% in March 2022, and a 0.4-percentage point decrease compared to 3% in February 2023.

CoreLogic has released its monthly Loan Performance Insights Report for March 2023, which found that 2.6% of all mortgages nationwide were in some stage of delinquency (defined as 30 days or more past due, including those in foreclosure), representing a 0.3-percentage point decrease, compared to 2.9% in March 2022, and a 0.4-percentage point decrease compared to 3% in February 2023.

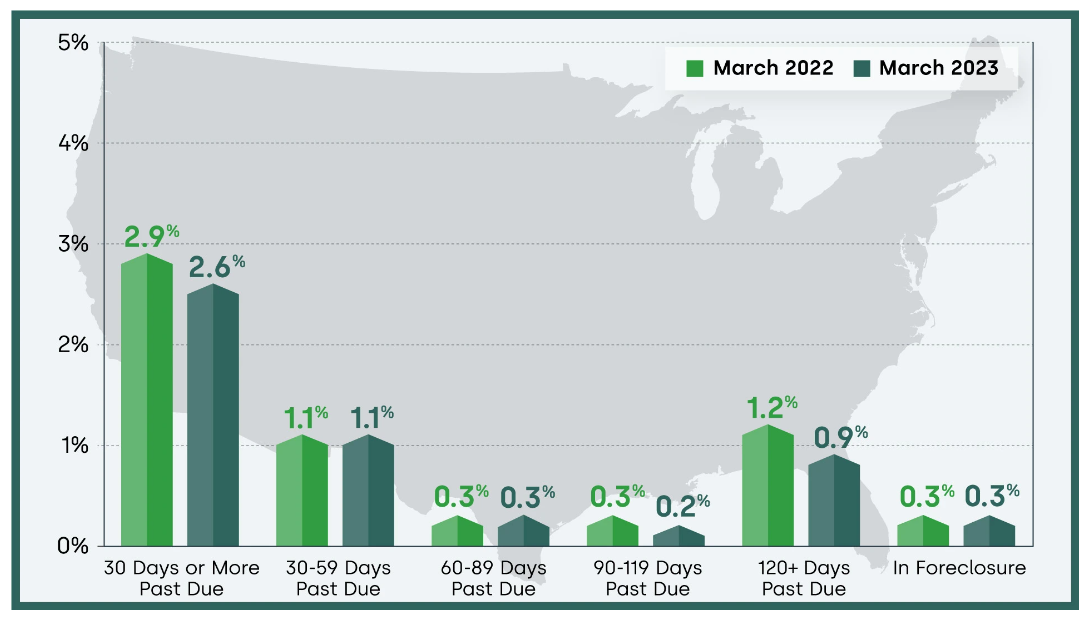

In breaking down the data, CoreLogic examined all stages of delinquency. In March 2023, the U.S. delinquency and transition rates and their year-over-year changes were as follows:

- Early-stage delinquencies (30 to 59 days past due):1%, unchanged from March 2022

- Adverse delinquency (60 to 89 days past due):3%, unchanged from March 2022.

- Serious delinquency (90 days or more past due, including loans in foreclosure):1%, down from 1.5% in March 2022 and a high of 4.3% in August 2020.

- Foreclosure inventory rate (the share of mortgages in some stage of the foreclosure process):3%, unchanged from March 2022.

- Transition rate (the share of mortgages that transitioned from current to 30 days past due):5%, unchanged from March 2022.

The overall U.S. mortgage delinquency rate declined to a new low in March, buoyed by an exceptionally strong job market. Despite regular news of major layoffs—primarily in the tech sector—April’s 3.4% unemployment rate remains near an all-time low, indicating that many workers who recently lost jobs were able to quickly find new positions.

Nationwide, serious delinquencies also dropped to the lowest level in more than two decades in March, while foreclosures also remained near a historic low. As in previous months, several metro areas on Florida’s Gulf Coast continue to see elevated serious delinquency rates as a result of the lingering effects of last fall’s Hurricane Ian.

“The U.S. mortgage delinquency rate fell to a historic low in March, reflecting the lowest U.S. unemployment rate in more than 50 years,” said Molly Boesel, Principal Economist for CoreLogic. “While a slowing economy could cause increases in job losses and mortgage delinquencies, years of home equity gains will provide borrowers who fall behind on their payments with a cushion. This equity should protect many homeowners from foreclosures. There is no current projection that the U.S. foreclosure rate will reach the same level as it did during the housing crisis more than a decade ago.”

Regionally, CoreLogic found that no state posted an annual increase in overall delinquency rates in March. The states with the largest declines were Alaska (down by 0.9 percentage points) and New York (down by 0.8 percentage points).

In March 2023, 20 U.S. metro areas posted an increase in overall delinquency rates. Cape Coral-Fort Myers, Florida (up by 1.3 percentage points) led, followed by Punta Gorda, Florida (up by 1.1 percentage points) and Bloomsburg-Berwick, Pennsylvania (up by 0.7 percentage points).

All but three U.S. metro areas posted at least a small annual decrease in serious delinquency rates (defined as 90 days or more late on a mortgage payment) in February. The metros that saw serious delinquencies increase were Cape Coral-Fort Myers, Florida (up by 1.1 percentage points), Punta Gorda, Florida (up by one percentage point) and Bloomsburg-Berwick, Pennsylvania (up by 0.1 percentage point).