DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

A new study from the Urban Institute finds that increased use of Housing Choice Vouchers (HCV) could significantly reduce the racial gap between Black and white homeownership.

The study—conducted by The Urban Institute in partnership with Urban Strategies Inc. (USI) and funded by JP Morgan Chase—found that more HCVs may help reduce the racial disparity in homeownership, which now sits at its highest in 50 years. A key change would allow households with an HCV use it for mortgage payments rather than rent.

One major contributor is the disproportionate burden that mortgage costs place on Black potential homebuyers. Inequity in income, along with structural racist policies, leads to nearly half of all of the vouchers going to Black non-Hispanic households.

A summary concluded that successful implementation requires collaboration between housing agencies, lenders, and other first-time-homebuyer programs.

Historically, discrimination has caused a disparity in access to home ownership and its benefits. Living in inadequate housing requires more upkeep and paying relatively more in property taxes. Legacies of redlining and current discriminatory lending have also hampered Black households' efforts to gain access to quality housing.

Key findings of the study include:

- The HCV home ownership program is limited in size and scope.

- The use of homeownership vouchers is higher in places with lower housing costs and lower fair market rent.

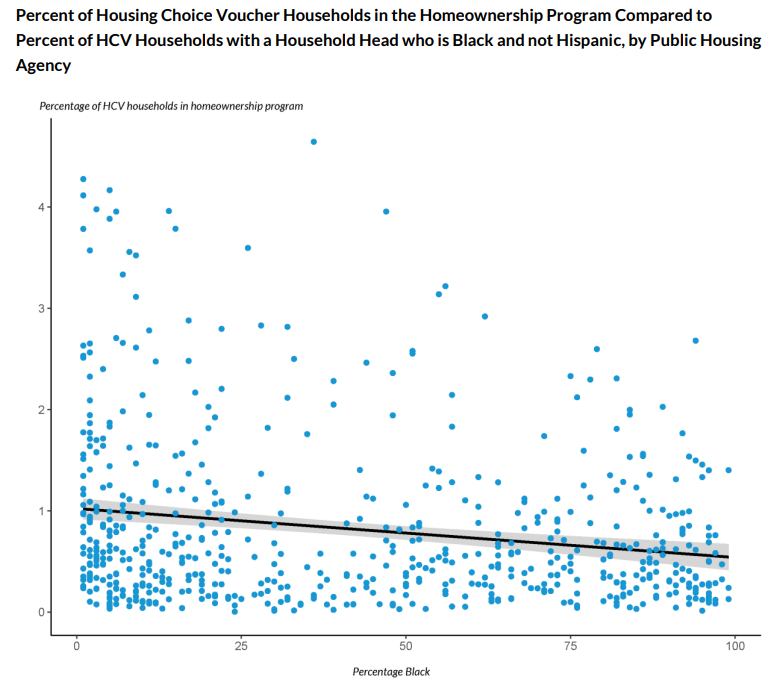

- Public housing authorities that use the highest share of vouchers for home ownership tend not to have majority Black non-Hispanic clientele. However, four out of five of the PHAs with the most participants serve majority Black non-Hispanic households in their programs: Philadelphia, Chicago, New Orleans, and Louisville.

- Foreclosures and non-payment are uncommon.

Strategies that the study said could help close the voucher gap include higher income limits for participants, creation of a distinct class of vouchers earmarked for homeownership, extending the length of subsidy allowed in the HCV homeownership program and more funding for the lump sum and/or down payment option.

No one policy or program is likely capable of closing the Black-white homeownership gap, which will take adding nearly five million African American homeowners nationwide. Researchers and policymakers are therefore exploring policies to make housing more affordable, strengthen government mortgage programs, and reduce renters’ barriers to homeownership.

To read the full analysis for more data, charts, and methodology, click here.