DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

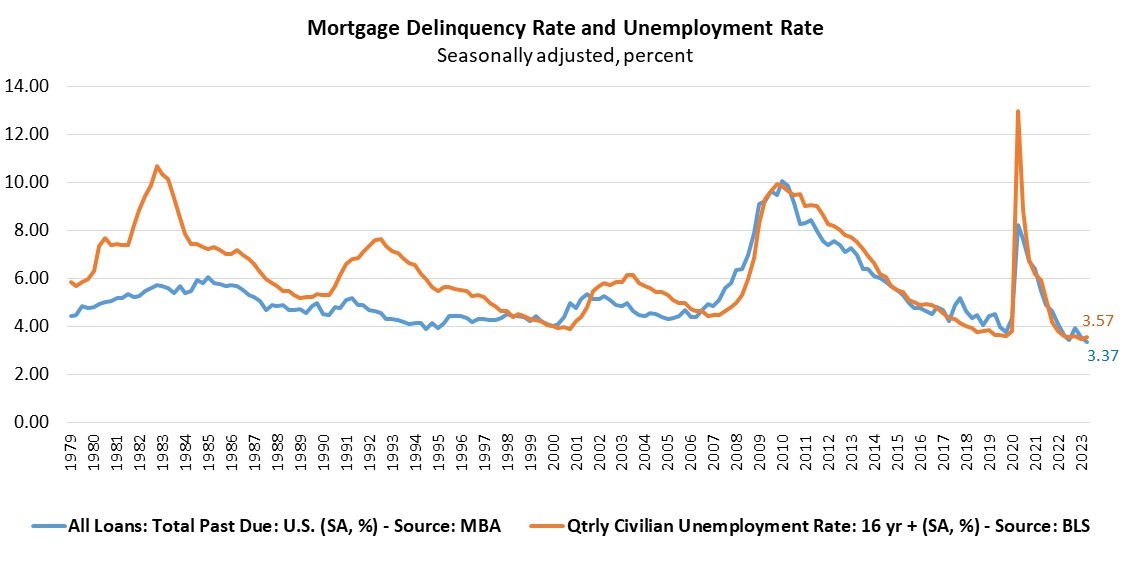

According to the Mortgage Bankers Association’s (MBA) National Delinquency Survey covering the second quarter of 2023, the delinquency rate for mortgage loans on one- to four-unit residential properties decreased to a seasonally adjusted rate of 3.37% of all loans outstanding.

According to the Mortgage Bankers Association’s (MBA) National Delinquency Survey covering the second quarter of 2023, the delinquency rate for mortgage loans on one- to four-unit residential properties decreased to a seasonally adjusted rate of 3.37% of all loans outstanding.

The delinquency rate was down 19 basis points from Q1 of 2023, and down 27 basis points year-over-year. The percentage of loans on which foreclosure actions were started in Q2 fell by three basis points to 0.13%.

“The seasonally-adjusted mortgage delinquency rate fell to its lowest level since MBA’s survey began in 1979, reaching 3.37% in the second quarter of 2023,” said Marina Walsh, CMB, MBA’s VP of Industry Analysis. “Buoyed by a resilient job market, homeowners are continuing to make their mortgage payments.”

Compared to Q1, the seasonally adjusted mortgage delinquency rate decreased for all loans outstanding. By stage, the 30-day delinquency rate decreased two basis points to 1.75%, the 60-day delinquency rate remained unchanged at 0.55%, and the 90-day delinquency bucket decreased 17 basis points to 1.07%.

By loan type, the total delinquency rate for conventional loans decreased 15 basis points to 2.29% over the previous quarter to the lowest level in the history of the survey dating back to 2004. The FHA delinquency rate decreased 32 basis points to 8.95%, and the VA delinquency rate decreased by 28 basis points to 3.70% over the previous quarter to the lowest level since Q4 of 2019.

On a year-over-year basis, total mortgage delinquencies decreased for all loans outstanding. The delinquency rate decreased by 35 basis points for conventional loans, increased 10 basis points for FHA loans and decreased 52 basis points for VA loans from the previous year.

The delinquency rate includes loans that are at least one payment past due but does not include loans in the process of foreclosure. The percentage of loans in the foreclosure process at the end of Q2 was 0.53%, down four basis points from Q1 of 2023, and six basis points lower than one year ago.

The non-seasonally adjusted seriously delinquent rate, the percentage of loans that are 90 days or more past due or in the process of foreclosure, was 1.61%, the lowest level since Q2 of 2000. It decreased by 12 basis points from the last quarter, and fell by 51 basis points from last year. The seriously delinquent rate decreased 10 basis points for conventional loans, decreased 30 basis points for FHA loans, and decreased 11 basis points for VA loans from the previous quarter. Compared to a year ago, the seriously delinquent rate decreased by 44 basis points for conventional loans, decreased 93 basis points for FHA loans, and decreased 68 basis points for VA loans.

“Despite low delinquency rates, there are early signs of possible consumer credit stress,” added Walsh. “Delinquencies are rising for other forms of credit, such as credit cards and car loans. In addition, FHA delinquencies rose 10 basis points compared to year ago levels. On a non-seasonally adjusted basis, FHA delinquencies rose 13 basis points year-over-year, and 71 basis points from the first quarter of 2023. As the economy slows and labor market cools, homeowners with FHA loans are likely to feel the distress first.”

The five states reporting the largest quarterly increases in their overall non-seasonally adjusted delinquency rate were:

- Indiana (37 basis points)

- Michigan (35 basis points)

- Ohio (35 basis points)

- Pennsylvania (32 basis points)

- Texas (31 basis points)

For the week ending August 5, the U.S. Department of Labor (DOL) reported the advance figure for seasonally adjusted initial unemployment claims was 248,000, an increase of 21,000 from the previous week's unrevised level of 227,000. The four-week moving average was 231,000, an increase of 2,750 from the previous week's unrevised average of 228,250. The advanced seasonally adjusted insured unemployment rate was 1.1% for the week ending July 29, unchanged from the previous week's unrevised rate.

“Total non-farm payroll employment increased by 187,000 in July and the unemployment rate changed little at 3.5%,” added First American Economist Ksenia Potapov. “June’s job report gains were revised down by 77,000, from 209,000 to 185,000, and May’s report was revised down by 25,000. Employment in May and June combined is 49,000 lower than previously reported.”

In terms of the impact on employment numbers on the housing space, Potapov added, “As existing homeowners remain rate-locked into their homes with no financial incentive to move, they are likely to increasingly turn to renovating their homes to suit their evolving needs.”