DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Experts have reported that the continually warming housing market is showing signs of a typical late-summer seasonal cooldown, according to the latest Zillow market report.

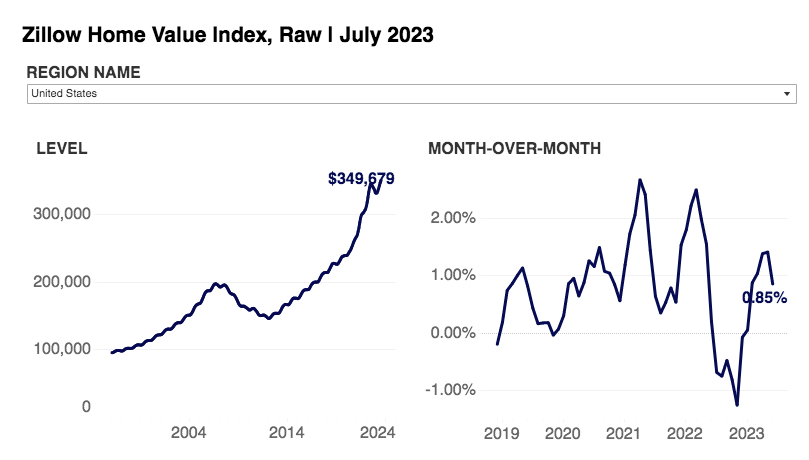

While home prices have increased in nearly all major U.S. markets, the typical U.S. home value climbed 0.9% from June to July.

As competition remains strong, housing inventory is hitting new lows for this time of year, leaving homebuyers more time to find and consider their home purchase.

Key Findings:

- Houses are spending more time on the market than in the spring, but still half as long as in 2019.

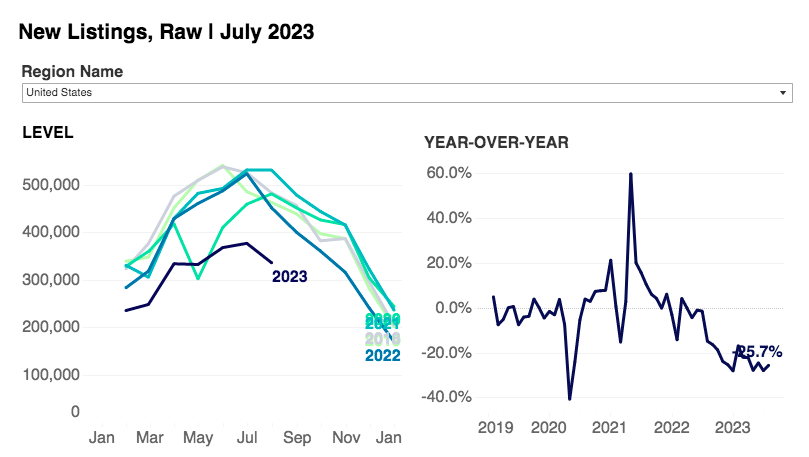

- Buyers still have few choices for existing homes as inventory reached new record lows for July.

- Home values rose from June to July in every major metro area except Austin.

"The housing market is returning to normal seasonal patterns, and that's a positive sign for buyers who faced stiff competition this spring," said Zillow Senior Economist Nicole Bachaud. "As summer winds down and kids head back to school, home shopping gets put on the back burner. Traditionally, buyers who remain in the market gain a bit more bargaining power heading into the fall. This year, however, sellers are sticking to the sidelines, which means even fewer options and high prices."

The typical U.S. home value climbed 0.9% from June to July—a steamy pace for this time of year, but a step back from 1.4% growth in the two preceding months. The nation's typical home value is now $349,679, which is 1.4% higher than last July and 46% above pre-pandemic levels in February 2020.

Austin was the only major market in which home values dipped from June to July, falling 0.5%.

The slowest monthly home value growth was in San Antonio (0.2%), Denver (0.2%), Birmingham (0.3%), and Memphis (0.3%).

Slowing sales give buyers a bit of breathing room

Easing monthly appreciation is one sign that the normal seasonal pendulum of the market is swinging back in favor of buyers. Homes are also spending longer on the market before going under contract—12 days in July compared to 11 in June and 10 in April and May.

The volume of newly pending sales also slowed down along seasonal trend lines, falling about 6.5% from June to July. Sales of existing homes, constrained by affordability challenges and a lack of homes on the market, are down about 15% year-over-year.

The number of listings with a price cut ticked up slightly from June as well. The share is right in line with pre-pandemic norms at about 22%.

Inventory drought marches on amidst high mortgage rates

Total active inventory in July was down 15% from last year and a tremendous 44% below July 2019 levels.

"Buyers should not expect to see many more homes available for sale on Zillow at any time this year than they do now," said Bachaud. "Inventory will decline from here if it follows pre-pandemic trends."

New research finds that homeowners are stubbornly holding on to their houses. New listings of existing homes have once again set a new seasonal low-water mark, as roughly 336,000 came to market in July. That's 26% fewer than last July and 41% below pre-pandemic averages.

New listings have been scarce for a year, and high mortgage rates remain the most likely reason. A recent Zillow survey found some evidence that the gap between homeowners' existing mortgage rates and today's rates can help explain their reluctance to sell: Owners with a rate of 5.0% or above were almost twice as likely to consider selling their homes in the next three years than those with a rate below 5%.

That doesn't mean rates need to return all the way to 5%, but that the lower they go, the more homeowners will be willing to entertain the idea of selling their homes to move.

Rents are climbing slightly faster than normal for July

After its own record-breaking run that saw annual rent price growth peak at 16% in February of 2022, the rental market is also falling back into more normal long-term patterns of growth, according to Zillow's latest rental market report.

The report also revealed July's 0.5% monthly rent growth was slightly hotter than pre-pandemic averages, but year-over-year growth of 3.6% was just a touch cooler.

Among the 50 largest metropolitan areas, rents rose the most on a monthly basis in Buffalo (1.4%), Virginia Beach (0.8%), Washington, DC (0.8%), Birmingham (0.8%), and New York City (0.8%).

To read the full report, including more data, charts, and methodology, click here.