DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

The Fannie Mae Home Purchase Sentiment Index (HPSI) decreased by 2.4 points in September to 64.5, as elevated mortgage rates further dampened already-pessimistic consumer housing sentiment. Five of the HPSI’s six components decreased month over month, including the components measuring perceived homebuying and home-selling conditions.

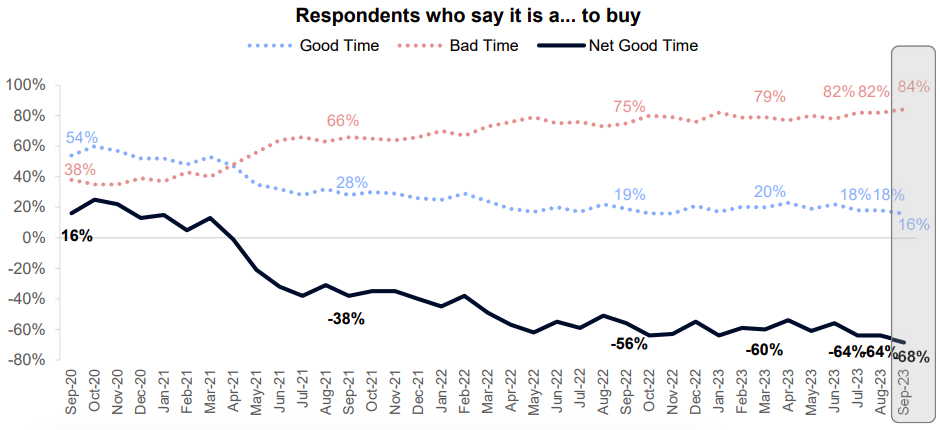

According to the report, in September, some 16% of consumers reported that it’s a good time to buy a home, matching the all-time survey low set last year. Additionally, an estimated 63% said it was a good time to sell a home, down 3 percentage points compared to the prior month. Only 17% of consumers indicated that they expect mortgage rates to go down over the next 12 months. Overall, the full index is up 3.7 points year-over-year.

“Mortgage rates persistently over 7 percent appear to be deepening the malaise consumers feel about the home purchase market,” said Doug Duncan, Fannie Mae Senior VP and Chief Economist. “In fact, high mortgage rates surpassed high home prices as the top reason why consumers think it’s a bad time to buy a home, a survey first. Notably, the share of consumers expressing pessimism about homebuying conditions hit a new survey high in September, with 84% now indicating that it’s a bad time to buy a home. On the sell side, respondents also listed unfavorable mortgage rates as the top reason why they believe it’s a bad time to sell a home. This indicates to us that many homeowners are probably not eager to give up their ‘locked-in’ lower mortgage rates anytime soon, but it also may reflect the worry of some homeowners that sale values might be suppressed slightly if the pool of qualified homebuyers is constrained by elevated mortgage rates.”

Home Purchase Sentiment Index – Component Highlights

Fannie Mae’s Home Purchase Sentiment Index (HPSI) decreased in September by 2.4 points to 64.5. The HPSI is up 3.7 points compared to the same time last year.

- Good/Bad Time to Buy: The percentage of respondents who say it is a good time to buy a home decreased from 18% to 16%, while the percentage who say it is a bad time to buy increased from 82% to 84%. As a result, the net share of those who say it is a good time to buy decreased 4 percentage points month over month.

- Good/Bad Time to Sell: The percentage of respondents who say it is a good time to sell a home decreased from 66% to 63%, while the percentage who say it’s a bad time to sell increased from 34% to 37%. As a result, the net share of those who say it is a good time to sell decreased 7 percentage points month over month.

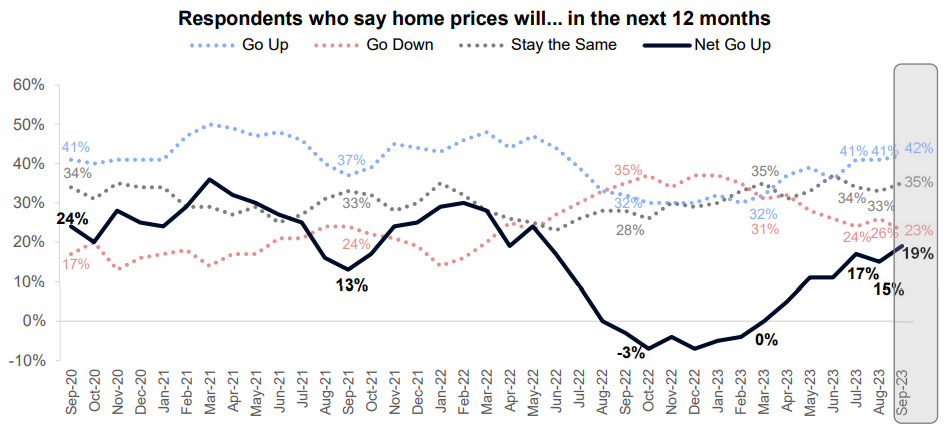

- Home Price Expectations: The percentage of respondents who say home prices will go up in the next 12 months remained increased from 41% to 42%, while the percentage who say home prices will go down decreased from 26% to 23%. The share who think home prices will stay the same increased from 33% to 35%. As a result, the net share of those who say home prices will go up in the next 12 months increased 4 percentage points month over month.

- Mortgage Rate Expectations: The percentage of respondents who say mortgage rates will go down in the next 12 months decreased from 18% to 17%, while the percentage who expect mortgage rates to go up remained unchanged at 46%. The share who think mortgage rates will stay the same increased from 34% to 37%. As a result, the net share of those who say mortgage rates will go down over the next 12 months decreased 1 percentage point month over month.

- Job Loss Concern: The percentage of respondents who say they are not concerned about losing their job in the next 12 months decreased from 78% to 75%, while the percentage who say they are concerned increased from 22% to 23%. As a result, the net share of those who say they are not concerned about losing their job decreased 3 percentage points month over month.

- Household Income: The percentage of respondents who say their household income is significantly higher than it was 12 months ago decreased from 22% to 18%, while the percentage who say their household income is significantly lower increased from 12% to 13%. The percentage who say their household income is about the same increased from 65% to 68%. As a result, the net share of those who say their household income is significantly higher than it was 12 months ago decreased 5 percentage points month over month.

“Consumers are also not seeing much affordability relief in sight, as they continue to expect home prices to increase in the next 12 months," said Duncan. "They also indicated that their personal economic situations are showing signs of strain, including lower year-over-year household incomes and a reduced sense of job security. In our view, all of this points to home purchase affordability remaining a problem for the foreseeable future, which we forecast will keep home sales sluggish into next year.”

To read the full report, including more data, charts, and methodology, click here.