DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Is 2024 the year that existing-home inventory will be unlocked or will the "sellers’ strike" continue?

A new study from First American revealed the surge in mortgage rates from mid-2022 through 2023 triggered a housing recession, with the most pronounced impact felt in a steep decline in sales—while prices have remained relatively stable.

Specifically, existing-home sales plunged to a more than 12-year low in September of this year. Rising mortgage rates have a dual impact on the housing market, reducing affordability for homebuyers and strengthening the rate lock-in effect for potential sellers.

October 2023 Potential Home Sales:

For the month of October, First American Data & Analytics updated its proprietary Potential Home Sales Model to show that:

- Potential existing-home sales decreased to a 5.26 million seasonally adjusted annualized rate (SAAR), a 1.0% month-over-month decrease.

- This represents a 50.8% increase from the market potential low point reached in February 1993.

- The market potential for existing-home sales increased 1.8% compared with a year ago, a gain of 95,000 (SAAR) sales.

- Currently, potential existing-home sales is 1,533,500 (SAAR), or 22.6%, below the peak of market potential, which occurred in April 2006.

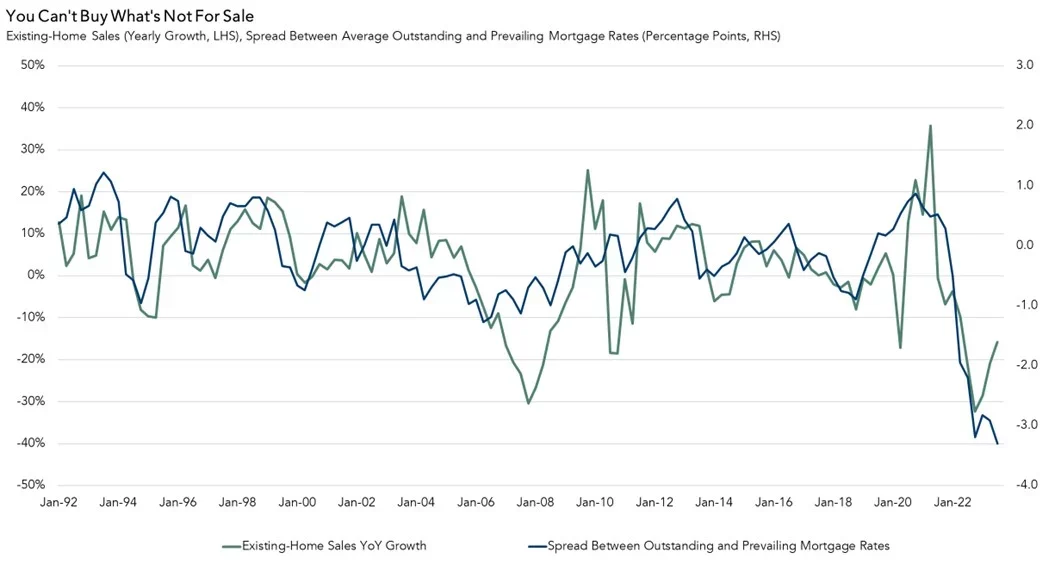

Historically, existing homes have made up nearly 90% of all for-sale inventory. However, in today’s housing market, more than 90% of homeowners are financially discouraged from selling their home because it would cost more to borrow the same amount of money they owe on their current mortgage. Potential homebuyers can’t purchase what’s not for sale, and existing homeowners aren’t selling.

The Blight, the Bright, and What Seems Just Right

The housing market of 2024 will likely present many of the same challenges as the market of 2023, but with the benefit of some added certainty from the Federal Reserve on its monetary policy. The Fed’s own projections indicate that the end of monetary tightening is close, if not already here. As a result of more certainty around Fed action, there could be some downward pressure on mortgage rates, or at the very least, some stability.

Industry consensus forecasts indicate that mortgage rates will end 2024 at 6.4%, which is a significant improvement over the peak of nearly 8% this year. If rates do come down from recent highs, the housing market may benefit, but headwinds will remain.

The Blight:

Unfortunately, even mortgage rates of 6.4% will not significantly alleviate the market from the rate lock-in effect, as 90% of homeowners are locked into rates below 6%. These existing homeowners will still withhold inventory from the market, which will put upward pressure on house prices and limit affordability. You can’t have more existing-home sales without more existing-home inventory. Even though mortgage rates may decline, it’s unlikely that it will be sufficient to end the sellers’ strike in 2024.

The Bright:

The October First American Data & Analytics Home Price Index indicated that house prices reached a new peak for the seventh month in a row last month. While higher house prices limit affordability, all else being equal, they also increase the equity cushion of existing homeowners.

Homeowner equity is already sitting near historic highs, and for some of those equity-rich homeowners, that means moving and taking on a higher interest rate isn’t a huge deal—especially if they are moving to a less expensive home. Additionally, 42% of owned homes are free and clear. These free-and-clear homeowners may hold the key to unlocking some much-needed supply for today’s housing market.

If mortgage rates do fall from the October 2023 rate of 7.6% to the consensus forecast of 6.4%, house-buying power will increase by nearly $42,000. Additionally, a large cohort of millennials are reaching prime buying age, and the post-pandemic new normal continues to offer greater flexibility to work from home, helping to fuel homeownership demand.

What Seems Just Right:

The pre-pandemic historic average for existing-home sales is approximately 5 million seasonally adjusted annualized (SAAR) sales. The latest data suggests that sales have declined below 4 million SAAR. The outlook for existing-home sales in 2024 is a modest improvement from 2023 levels, but not quite back to historic norms. Lower mortgage rates in 2024 will likely not be low enough to end the sellers’ strike entirely, but for those homeowners who do choose to sell, improved affordability for potential buyers means there will be someone to buy it at the right price.

To read the full report. including more data, charts, and methodology, click here.