DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

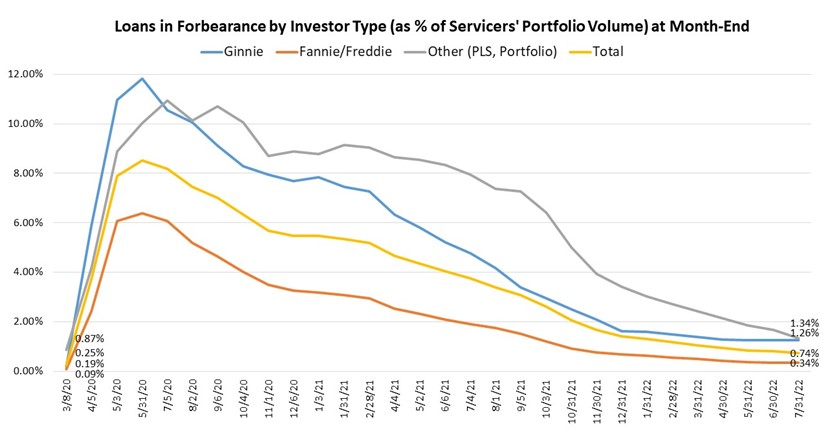

As the pandemic continues to grow smaller and smaller in our respective rearview mirrors, the number of loans in forbearance nationwide continues to shrink, as the Mortgage Bankers Association (MBA) reports that total decreased by seven basis points from 0.81% of servicers’ portfolio volume in the prior month, to 0.74% as of July 31, 2022.

As the pandemic continues to grow smaller and smaller in our respective rearview mirrors, the number of loans in forbearance nationwide continues to shrink, as the Mortgage Bankers Association (MBA) reports that total decreased by seven basis points from 0.81% of servicers’ portfolio volume in the prior month, to 0.74% as of July 31, 2022.

Nationwide, the MBA estimates that there are now just 370,000 homeowners currently in forbearance plans, down 35,000 from June 2022’s total of 405,000 homeowners in forbearance plans.

“July continued the ongoing trend in recent months of most of the forbearance exits coming from borrowers with portfolio loans and private label security loans,” said Marina Walsh, CMB, MBA’s VP of Industry Analysis. “There has been very little change in the forbearance rate for Fannie Mae, Freddie Mac, and Ginnie Mae loans during the past three months, perhaps indicating that we have reached a floor, with loans entering forbearance about equal to loans exiting forbearance for these loan types.”

As Walsh notes, the share of Fannie Mae and Freddie Mac loans in forbearance decreased just one basis point, falling from 0.35% to 0.34%, while Ginnie Mae loans in forbearance remained the same relative to the previous month at 1.26%. The forbearance share for portfolio loans and private-label securities (PLS) declined a bit more, dipping 34 basis points, from 1.68% to 1.34%.

By stage, 30.5% of total loans in forbearance were in the initial forbearance plan stage, while 56.1% were in a forbearance extension. The remaining 13.4% are forbearance re-entries, including re-entries with extensions.

As more exit forbearance, running parallel and trending positively as well is the nation’s employment numbers, as the U.S. Bureau of Labor Statistics (BLS) reported solid gains as well in July 2022, with total nonfarm payroll employment rising by 528,000, and the unemployment rate edging downward to 3.5%.

“July employment gains were led by hires in professional and business services, leisure and hospitality, and health care–consistent with recent trends,” said Realtor.com Senior Economic Research Analyst Joel Berner. “This month saw no change to the share of employees working remotely specifically because of the pandemic, maintaining at 7.1%. After increasing in June, July saw slightly more employees report that they were unable to work because their employer closed down because of the pandemic, up to 2.2 million in July compared to 2.1 million last month. July saw another improvement in terms of the pandemic’s effect on employment, as the number of people who are not in the labor force and were unable to look for work because of the pandemic fell from 610,000 to 548,000.”

Total completed loan workouts from 2020 and onward (repayment plans, loan deferrals/partial claims, loan modifications) that were current as a percent of total completed workouts declined to 78.82% in July 2022, down from 81.34% in June 2022.

Loans in forbearance as a share of servicing portfolio volume (#) as of July 31, 2022:

- Total: 0.74% (previous month: 0.81%)

- Independent Mortgage Banks (IMBs): 1.00% (previous month: 1.03%)

- Depositories: 0.56% (previous month: 0.62%)

Of the cumulative forbearance exits for the period from June 1, 2020, through July 31, 2022, at the time of forbearance exit:

- 29.5% resulted in a loan deferral/partial claim.

- 18.5% represented borrowers who continued to make their monthly payments during their forbearance period.

- 17.2% represented borrowers who did not make all of their monthly payments and exited forbearance without a loss mitigation plan in place yet.

- 15,8% resulted in a loan modification or trial loan modification.

- 11.1% resulted in reinstatements, in which past-due amounts are paid back when exiting forbearance.

- 6.7% resulted in loans paid off through either a refinance or by selling the home.

- 1.2% resulted in repayment plans, short sales, deed-in-lieus or other reasons.

Regionally, the five states reporting the highest share of loans that were current as a percent of servicing portfolio included:

- Idaho

- Washington

- Colorado

- Utah

- Oregon

On the other end of the spectrum, the five states with the lowest share of loans that were current as a percent of servicing portfolio included:

- Mississippi

- Louisiana

- New York

- West Virginia

- Indiana