DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Contrary to some reports in the mortgage industry that customer experience investments are unnecessary and unprofitable, a study from J.D. Power indicates that investing in the customer experience does pay off for mortgage servicers.

Contrary to some reports in the mortgage industry that customer experience investments are unnecessary and unprofitable, a study from J.D. Power indicates that investing in the customer experience does pay off for mortgage servicers.

J.D. Power’s 2016 Primary Mortgage Servicer Satisfaction Study, released on Thursday, indicates that investments in the customer experience can lead to both increased profits and greater customer satisfaction. The study measured customer satisfaction with the mortgage servicing experience in six factors: new customer orientation; billing and payment process; escrow account administration; interaction; mortgage fees; and communications.

“Servicers with a captive audience can often view taking measurable steps that improve the customer experience as an unnecessary investment,” said Craig Martin, senior director of the mortgage practice at J.D. Power. “They aren't against improving satisfaction, but cost containment is their top priority. The study clearly shows, however, that interacting with customers more efficiently—and more effectively—can reduce costs and increase profit for servicers regardless of the business model, while having the added bonus of improving satisfaction.”

The perception that strategically investing in the customer experience is ineffective possibly stems from the fact that many customers do not choose their servicers; 48 percent of customers said they did not, according to the study. Also, many barriers exist prevent customers from changing servicers.

Servicers can benefit from investing in the customer experience in four ways, according to the study:

- Complaint reduction—When servicers allow customers to receive answers to questions without a phone call (i.e. via the website) or on a single call, it reduces the number of repeated customer contacts that can escalate into regulatory scrutiny.

- Cost containment and reduction—Eliminating the need for customers to contact and increasing the use of self-service channels reduces customers’ reliance on the live phone channel.

- Limiting portfolio loss—Delivering a satisfying customer experience will greatly improve the chances that customers will consider the lender for future mortgage needs, which in turn can reduce acquisition costs, thus supporting future revenue growth. According to the study, 63 percent of customer said they would switch servicers if customer satisfaction level was below 600 (on a 1,000-point scale; conversely, if a servicer’s customer satisfaction level is above 900, 66 percent of customers said they would “definitely” use their current servicer to refinance.

- Developing new business opportunities—A satisfying experience for customers provides increased cross-sell of existing customers, and also leads to more new business with partners.

The study showed that customers are likely to call their servicer when there is a problem (83 percent), which could potentially lead to regulatory scrutiny, since 13 percent of customers said they post their problems on social media. When problems are eliminated, it goes right to the bottom line by reducing call center costs and also reducing the risk and costs associated with unwanted scrutiny from regulators.

The study showed that customers are likely to call their servicer when there is a problem (83 percent), which could potentially lead to regulatory scrutiny, since 13 percent of customers said they post their problems on social media. When problems are eliminated, it goes right to the bottom line by reducing call center costs and also reducing the risk and costs associated with unwanted scrutiny from regulators.

There was a substantial reduction in calls to live agents (42 percent to 30 percent) when a company has an easy-to-navigate website with useful information, according to the study; in fact, 40 percent of customers said they searched the servicer’s website prior to calling, indicating that they prefer using self-service options before resorting to a phone call.

“Most servicers tend to focus on the complaints they receive, but the truly successful servicers get to the root causes of problems and take a more proactive approach,” Martin said. “They realize better communication and self-service options can help their bottom line by reducing unnecessary calls.”

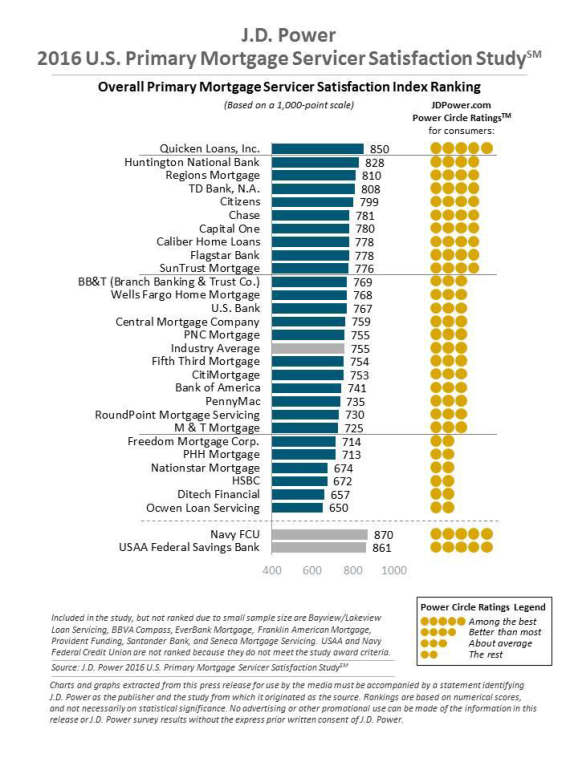

The study was based on responses (fielded from March through April 2016) from 7.542 customers who have had a mortgage on their primary residence for at least one year. On a 1,000-point scale, Quicken Loans ranked highest in the study with a score of 850, followed by Huntington National Bank (828) and Regions Mortgage (810), the latter of which improved its score by 77 points from 2015.