DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

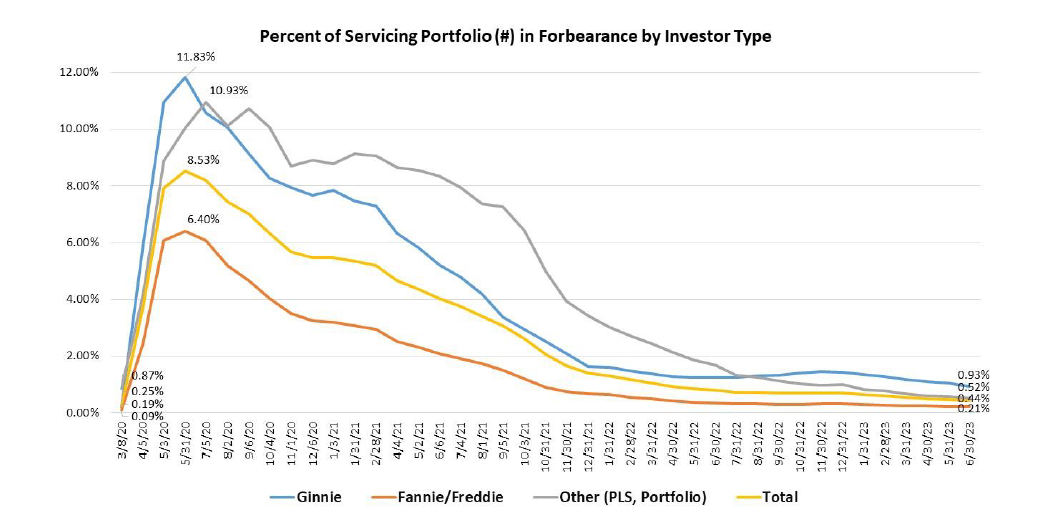

The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance continued to fall in June, decreasing five basis points from 0.44% of mortgage servicers’ portfolio volume in May 2023 to 0.49% as of June 30, 2023.

The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance continued to fall in June, decreasing five basis points from 0.44% of mortgage servicers’ portfolio volume in May 2023 to 0.49% as of June 30, 2023.

The MBA estimates that 220,000 homeowners are currently in forbearance plans, and nationwide, mortgage servicers have provided forbearance plans to approximately 7.9 million borrowers since March 2020.

In June 2023, the share of Fannie Mae and Freddie Mac (GSE) loans in forbearance decreased two basis points from 0.23% to 0.21%. Ginnie Mae loans in forbearance decreased 13 basis points from 1.06% to 0.93%, and the forbearance share for portfolio loans and private-label securities (PLS) decreased six basis points from 0.58% to 0.52%.

“Mortgage forbearance has declined because most homeowners have maintained or improved their financial health,” said Marina B. Walsh, CMB, MBA’s VP of Industry Analysis. “Recent reporting by the U.S. Bureau of Labor Statistics shows continued job growth in June, and a 3.6% unemployment rate. The employment situation tracks with homeowners’ ability to make mortgage payments.”

When stating the reason for their forbearance, 78.3% of borrowers stated they were in forbearance due to COVID-19-related reasons. Another 6.1% were in forbearance due to a natural disaster. The remaining 15.6% of borrowers are in forbearance for other reasons, such as a temporary hardship caused by job loss, death, divorce, disability, etc.

By stage, 34.9% of total loans in forbearance were in an initial forbearance plan stage, while 54.5% were in a forbearance extension. The remaining 12.6% were forbearance re-entries, including re-entries with extensions.

Of the cumulative forbearance exits for the period from June 1, 2020, through June 30, 2023, at the time of forbearance exit:

- 29.5% resulted in a loan deferral/partial claim.

- 17.9% represented borrowers who continued to make their monthly payments during their forbearance period.

- 17.9% represented borrowers who did not make all of their monthly payments and exited forbearance without a loss mitigation plan in place yet.

- 16.1% resulted in a loan modification or trial loan modification.

- 10.8% resulted in reinstatements, in which past-due amounts are paid back when exiting forbearance.

- 6.6% resulted in loans paid off through either a refinance or by selling the home.

- The remaining 1.2% resulted in repayment plans, short sales, deed-in-lieus or other reasons.

The five states reporting the highest share of loans that were current as a percent of servicing portfolio:

- Washington

- Idaho

- Colorado

- Oregon

- California

The five states reporting the lowest share of loans that were current as a percent of servicing portfolio:

- Mississippi

- Louisiana

- New York

- Indiana

- West Virginia

In its recently issued Mortgage Metrics Report for Q1 of 2023—providing information on mortgage performance through March 31, 2023—the Office of the Comptroller of the Currency (OCC) reported an improvement in the performance of first-lien mortgages in the federal banking system compared to the previous quarter. As of March 31, 2023, the reporting banks serviced approximately 12 million first-lien residential mortgage loans with $2.7 trillion in unpaid principal balances. This $2.7 trillion represented 22% of all residential mortgage debt outstanding in the United States.

Overall mortgage performance in Q1 improved from Q1 of 2022. The percentage of mortgages that were current and performing at the end of the Q1 of 2023 was 97.6% compared with 96.9% at the end of Q1 of 2022.

The CARES Act, signed into law on March 27, 2020, and extended on February 18, 2022, allows for loan forbearance that can extend up to 360 days, and is reflected in the mortgage performance data.

“MBA forecasts a slowing in the economy that could give rise to higher unemployment and mortgage delinquencies later in the year,” added Walsh. “Forbearance remains a viable loss mitigation option for homeowners who may struggle under more challenging economic conditions.”