DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Doug Duncan, Fannie Mae’s SVP and Chief Economist, has authored a new blog post on the topic of loan costs and the efficacy of recent technology investments considering the state of transition the market as it combats both inflation and rising rates.

Doug Duncan, Fannie Mae’s SVP and Chief Economist, has authored a new blog post on the topic of loan costs and the efficacy of recent technology investments considering the state of transition the market as it combats both inflation and rising rates.

Citing data from Fannie Mae, Duncan said that there are mounting affordability constraints for consumers, demand for home purchase and refinance mortgages has declined meaningfully over the past year, and this trend is expected to continue through 2023.

In addition, loan origination profitability tanked in 2022, as average production costs rose to a new high. In response to the additional stress on their balance sheets, some mortgage lending firms have announced layoffs, ceased specific products, or shuttered all together.

According to Fannie Mae’s most recent Mortgage Lender Sentiment Survey (MLSS), which surveyed well-placed economists and lenders on what changes are driving the increase in loan origination costs, and their views on the impact of recent digitization efforts on cost efficiency.

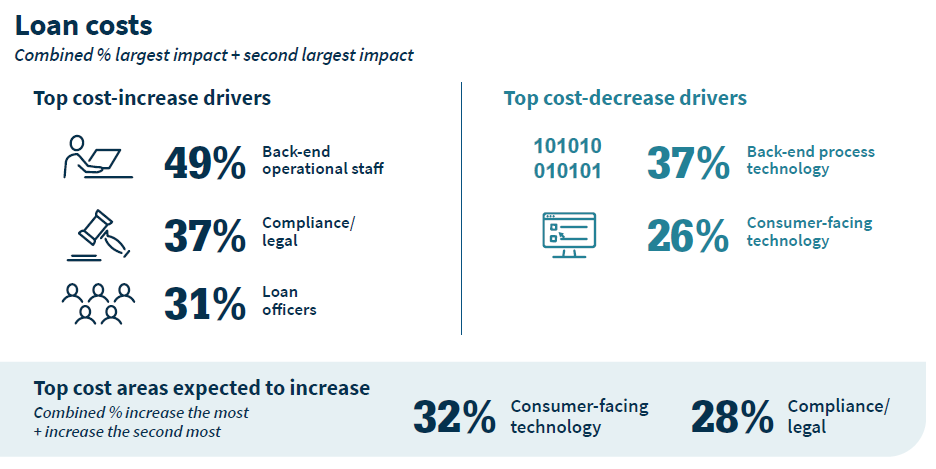

“Surveyed lenders cited personnel expenses as the primary factors driving up loan origination costs over the past two years,” Duncan said. “Further, they noted that investment in digitization was less effective at reducing costs—or in converting them from fixed to variable—even though, for most, it helped improve the consumer experience and reduce cycle time and error rates.”

Overall, lenders reported that personnel costs, compliance/legal, and individual loan officers were the top categories that increase average loan costs. In relation to digitization investments, including in back-end processing and consumer-facing technology, were the categories that were driving down loan costs.

Nearly all lenders have invested in digitization efforts over the past two years in one way or another due to the COVID-19 pandemic, not all lenders saw a return on investment over the last two years. Seven percent of lenders reported “significant” cost savings, while 52% indicated a modest amount of savings.

Many lenders also pointed out that they invested in technology to meet shifting consumer preferences, and that a positive return on investment was not necessarily the primary goal.

Lenders were also asked about any plans of outsourcing American workers to manage costs; 80% of lenders reported that they have, and will continue to, keep loan originations in-house. However, for those that have outsourced jobs, 80% found it was a viable strategy to convert fixed costs to variable costs.

“Given lenders' acknowledgment that technology and legal/compliance costs are unlikely to be cut, many appear to be turning to payroll reduction to help manage costs,” Duncan said. “Employment among nonbanks and mortgage brokers remains relatively high today, compared to the pre-COVID era. With the market experiencing significant declines in loan volume and applications, productivity (in terms of average loan volume or applications per employee) has also dropped significantly, indicating there's potentially excess capacity.

“Recent news about layoffs, mortgage business closures, and mergers suggest that lenders are scaling back their production employment in response to the cooling housing market,” Duncan concluded. “With an industry consensus forecast of a 35- to 50% drop in origination volume in 2022, it's likely that many lenders will continue to right-size capacity to remain competitive.”

Click here to read Duncan’s blog post in its entirety.